New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring

The major tax legislation[1] enacted last December will cost approximately $1.5 trillion over the next decade and deliver windfall gains to wealthy households and profitable corporations, further widening the gap between those at the top of the income ladder and the rest of the nation.[2] By shrinking revenues, it will leave the nation less prepared to address the retirement of the baby boom generation and other national needs that will require more revenue. Moreover, the complex, hastily drafted legislation will likely trigger a surge in tax gaming that could pose a risk to the integrity of the U.S. tax system, as wealthy taxpayers and corporations exploit newly created loopholes that tax experts have already identified and uncover other loopholes that the hasty drafting unwittingly created.

This paper reflects analyses of the new law that were undertaken either during the final stages of the congressional debate or shortly after the legislation was signed into law. More analyses will surely be forthcoming as more tax experts scrutinize the law and how it is being applied. But it is already clear that the law has fundamental flaws. It confers enormous tax benefits on some industries but not others, makes it easier for wealthy households to shelter income from taxes, and favors business production and investment overseas rather than at home.

Policymakers should pursue true tax reform that avoids the regressiveness of this law and accords more favorable treatment to working people with low or modest incomes.Instead of pursuing minor fixes or technical corrections to the law, policymakers should set a new course and pursue true tax reform that avoids the regressivity of this law and accords more favorable treatment to working people with low or modest incomes; raises revenue to meet national needs; and improves economic efficiency and strengthens the integrity of the tax code.

This analysis examines the law’s three fundamental flaws:

1. It ignores the stagnation of working-class wages and exacerbates inequality. Income has shifted from the bottom and middle of the income distribution to the top in recent decades, as wages have been close to stagnant for many working families while rising sharply at the top. As a just-released Congressional Budget Office (CBO) analysis shows, the share of income flowing to the bottom 60 percent fell by 4.4 percentage points between 1979 and 2014, while the share flowing to the top 1 percent rose by 5.7 percentage points.

Instead of pushing back against this trend, the new tax law exacerbates it. In 2025, it will boost the after-tax incomes of households in the top 1 percent by 2.9 percent, roughly three times the 1.0 percent gain for households in the bottom 60 percent. The tax cuts that year will average $61,100 for top 1 percent — and $252,300 for the top one-tenth of 1 percent.

The new law’s heavy tilt to the top largely reflects several large provisions that primarily benefit the most well-off. Its core provision is a deep cut in the corporate tax rate, which will mostly benefit shareholders and highly compensated employees such as CEOs. The law also showers large tax benefits on heirs to multi-million-dollar estates, cuts the top income tax rate, and provides a special deduction for certain business owners who are disproportionately high income.

The economic circumstances of low- and moderate-income working families, in contrast, are largely an afterthought in the new law. For example, in last-minute changes to the bill, negotiators agreed to a deeper cut in the top individual tax rate but rejected calls from Senators Marco Rubio and Mike Lee to deliver more than a token increase of $75 or less in the Child Tax Credit to 10 million children in low-income working-class families. And lawmakers drafting the law apparently did not consider strengthening the Earned Income Tax Credit (EITC), which is well placed to be at the forefront of an effort to boost working-family incomes (see box).

The new law will also harm many working families. For example, its repeal of the Affordable Care Act’s (ACA) individual mandate — the requirement that most people enroll in health insurance coverage or pay a penalty — is expected to add millions to the ranks of the uninsured and increase insurance premiums in the individual market.

2. It weakens revenues at a time when the nation needs to raise more revenue. The new tax law will cost $1.5 trillion over the next decade, according to Joint Committee on Taxation (JCT) estimates. JCT also finds that the law will only modestly improve economic growth — enough to recoup only about one-quarter of these costs.

These large revenue losses are irresponsible given the fiscal challenges the nation will face over the next several decades due to an aging population, health care costs that likely will continue to rise faster than the economy, interest rates returning to more normal levels, potential national security threats, and current and emerging domestic challenges such as large infrastructure needs that cannot be deferred indefinitely. Because of these pressures, CBPP and other analysts project that spending will need to rise as a percentage of gross domestic product (GDP), with most of the spending growth concentrated in a few programs — Social Security, Medicare, and Medicaid — that have widespread public support and whose growth is traceable to demographic and health care cost factors, not to more generous coverage or benefits.

The nature and magnitude of these fiscal pressures will require revenue to rise as a percentage of GDP to prevent an unsustainable rise in the nation’s debt ratio over coming decades. The new tax law, however, pushes in the opposite direction.

3. It invites rampant tax gaming and risks undermining the integrity of tax code. True tax reform simplifies the tax code and narrows the gaps between how different types of income are taxed so that individuals and businesses base their economic decisions on economics, not taxes. The new law does the opposite, adding complexity to the tax code and introducing new, arbitrary distinctions between different kinds of income.

The law “has turned us into a nation of tax shelter hunters,” the Tax Policy Center’s (TPC) Howard Gleckman has observed, as various provisions of the law have “set off a frenzy of loop-hole seeking.”[3] Widespread abuse of tax shelters could cause the bill to lose even more revenue than official estimates of the law now show — and is likely to increase income inequality even more, since tax avoidance is worth the most to wealthy individuals and profitable corporations, who also are best equipped to take advantage of those opportunities.

- A prime example is the law’s 20 percent deduction for “pass-through” income, or income from businesses such as partnerships, S corporations, and sole proprietorships that business owners claim on their individual tax returns. The deduction effectively means that certain pass-through income will face a lower tax rate than wages and salaries, creating an incentive for high-income individuals to reclassify their salaries as pass-through income. While the new law includes complex “guardrails” intended to prevent such abuse, they are poorly designed. Tax experts have suggested, for example, that while highly paid doctors are not eligible for the pass-through-income deduction, a group of doctors could create a real estate pass-through company — which would be eligible for the deduction — and have the company own the medical practice’s building and charge extremely high rent, so that a significant portion of the doctors’ income would then accrue to that company and receive the deduction.

- The new law also creates a powerful incentive for wealthy Americans to shelter large amounts of income in corporations by slashing the corporate rate by two-fifths (from 35 percent to 21 percent), thereby opening up a wide gap between the top individual tax rate and the corporate rate. An investor with a multi-million-dollar bond portfolio would have an incentive to place it in a corporation and pay roughly half the tax rate on the interest income it produces that she’d pay if that income faced the individual tax rates. She might eventually have to pay taxes on the dividends or capital gains on the wealth that has accrued in the corporation, but she could defer that second layer of tax for decades and even avoid it altogether by passing the corporation housing her bond portfolio on to her heirs.

- The new law also moves U.S. international tax rules to a “territorial” system that largely exempts multinationals’ foreign profits from U.S. tax and thereby encourages them to shift profits and operations overseas. The drafters of the law put in place a minimum tax to limit this incentive, but it is seriously flawed and, as explained below, could in fact add to incentives to shift both paper profits and real investments and operations overseas.

New Law Heavily Tilted Toward Wealthy and Corporations

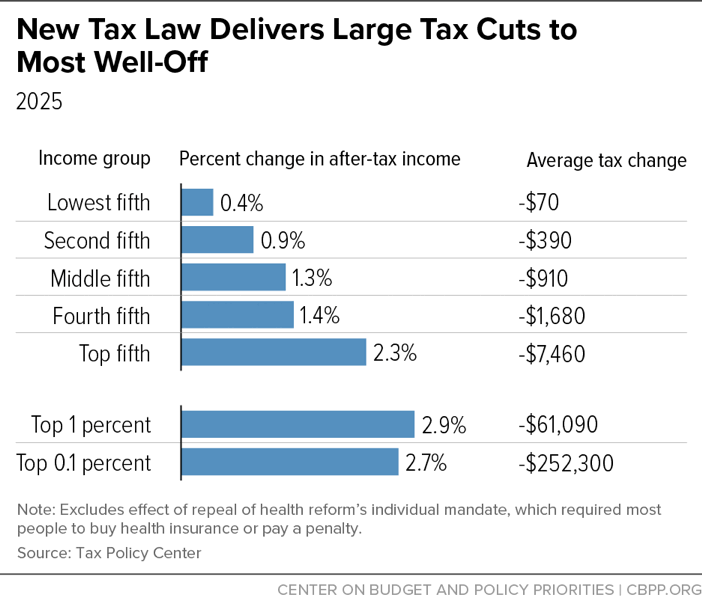

The new tax law will increase income inequality since it delivers far larger tax cuts to households at the top, measured as a share of income, than to households at the bottom or middle of the income distribution. In 2025, when the new law will be fully phased in and before many provisions in it are scheduled to expire, it will boost the after-tax incomes of households in the top 1 percent by 2.9 percent, or roughly triple the 1.0 percent gain for households in the bottom 60 percent, according to TPC.[4] Similarly, households in the top one-tenth of 1 percent (0.1 percent) will receive a 2.7 percent increase in after-tax income. (See Figure 1.)

The average tax cut that year for the top 1 percent — those with incomes above $837,800 — will be $61,100. Those in the top 0.1 percent — households making more than $4.7 million a year — will receive windfalls averaging $252,300. In stark contrast, the bottom 60 percent of households — those making under $91,700 — will receive about $400, on average. Notably, these numbers do not include the negative effects on some middle-income families from the law’s repeal of the ACA’s individual mandate, such as increasing the number of uninsured and raising premiums, as discussed below.

The new tax law will, therefore, add to the growing polarization of income and wealth of recent decades. As noted, the share of after-tax income flowing to the top 1 percent grew by 5.7 percentage points between 1979 and 2014 (the latest year for which these data are available), while the share of income going to the bottom 60 percent fell by 4.4 percentage points.[5] The economic environment has been particularly challenging for working-class households, defined here as those with working-age adults in which no one has a college degree. The after-tax income of a typical working-class family of three would be about $9,600 higher ($58,300 instead of $48,700) if its income had grown at the same rate since 1979 as that of a typical household with a college degree.[6]

Upward Tilt Reflects Law’s Core Provisions

Crafting the new tax law, which reallocates trillions of dollars, gave policymakers a rare opportunity to lean against rising inequality by strengthening the overall progressivity of the tax code and significantly boosting the after-tax incomes of working-class families. (See box on the Earned Income Tax Credit.) The final legislation that emerged not only fails to address this matter but makes it worse, mostly due to a handful of major provisions that lose considerable revenue while primarily benefiting wealthy households.[7] These include:

Cutting corporate taxes. The centerpiece of the new tax law is a cut in the corporate tax rate from 35 percent to 21 percent and a shift to a territorial tax system, in which multinational corporations’ foreign profits will largely no longer face U.S. tax. This large corporate tax cut contributes to the law’s skewed distribution, as it largely benefits corporate shareholders.[8] TPC estimates that a third of the benefits from corporate rate cuts will ultimately flow to the top 1 percent of households. Contrary to Trump Administration claims that these corporate tax cuts primarily benefit workers, mainstream economic research concludes that over 75 percent of the benefits go to shareholders instead. Further, even the modest part of a corporate rate cut that would flow to workers would likely do so in proportion to their share of total wage and salary income. A large portion of that income flows to CEOs and other highly paid executives; only a modest portion goes to workers in the middle and bottom, who have been hurt most by slow wage growth of recent decades.

Creating a 20 percent deduction for pass-through income. The new tax law creates a deduction for pass-through income that effectively cuts the marginal tax rate on this income by up to one-fifth. This provision is heavily tilted to the wealthy, for three reasons.[9] First, high-income households get a disproportionate share of pass-through income; the top 1 percent alone receives more than half. Second, pass-through income makes up a much larger share of income for high-income households than for the middle class. Third, each dollar of pass-through income that’s deducted is worth more as a tax break for high-income people, since they face the highest regular individual tax rates.

This provision could deliver even more tax cuts concentrated on the very wealthy if it leads to large-scale tax avoidance, since highly paid individuals will have the biggest incentive and ability to try to reclassify their wage and salary income as pass-through income to take advantage of the deduction (as discussed in more detail in the last section of this analysis).

Doubling the estate tax exemption. The law doubles the amount that the wealthiest households can pass on tax-free to their heirs, from $11 million per couple to $22 million, or many times the lifetime earnings of a typical high school graduate.[10] The few estates large enough to remain taxable — those worth more than $22 million per couple — will receive a tax cut of $4.4 million apiece. This new estate tax cut will cause even more wealth to go untaxed than under prior law, since much of the wealth it exempts from the tax consists of “unrealized” capital gains that have never been taxed, and those who inherit the money won’t have to pay income tax on these windfalls.[11] (The increase in the estate tax exemption could also discourage work among some wealthy heirs working by giving them even larger inheritances, contrary to the pro-work rhetoric of the new law’s proponents.[12])

Cutting the top individual income tax rate to 37 percent. The new law cuts the top individual income tax rate from 39.6 percent to 37 percent for married couples with over $600,000 in taxable income. By itself, this rate cut will give a couple with $2 million in taxable income a $36,400 tax cut each year.[13] Wealthy households will also benefit from the law’s cuts in the other individual rates. Altogether, the changes in tax rates alone are worth a tax cut of $56,765 for a married couple with $2 million in taxable income.

Weakening the Alternative Minimum Tax (AMT). The AMT is a parallel tax system designed to ensure that higher-income people who take large amounts of deductions and other tax breaks pay at least a minimum level of tax. The new law significantly weakens the AMT by raising both the amount of income that’s exempt from the tax (from $86,200 to $109,400 for a married couple) and the income level above which this exemption begins phasing out (from $164,100 to $1 million for a married couple). The overall effect is a further tax cut for affluent households.

Law Does Relatively Little for Working- and Middle-Class Americans

Working families seemed largely an afterthought in congressional deliberations over the new tax law. Key tax parameters that affect these families change significantly under the law, but often in offsetting ways.

Proponents of the law frequently highlight its rate cuts, increase in the standard deduction, and doubling of the Child Tax Credit (CTC) for some families (see below). Yet other provisions raise taxes on families, such as the elimination of personal exemptions and the new inflation adjustment for key tax parameters, which will push more taxpayers into higher tax brackets over time. The end result is only modest tax cuts overall for working- and middle-class families, which pale in comparison to the large net tax cuts for wealthy households and profitable corporations. In addition, TPC analysis finds that an estimated 21 percent of households making under $200,000 will see no tax cut or even tax increases in 2018 under the new law.[14]

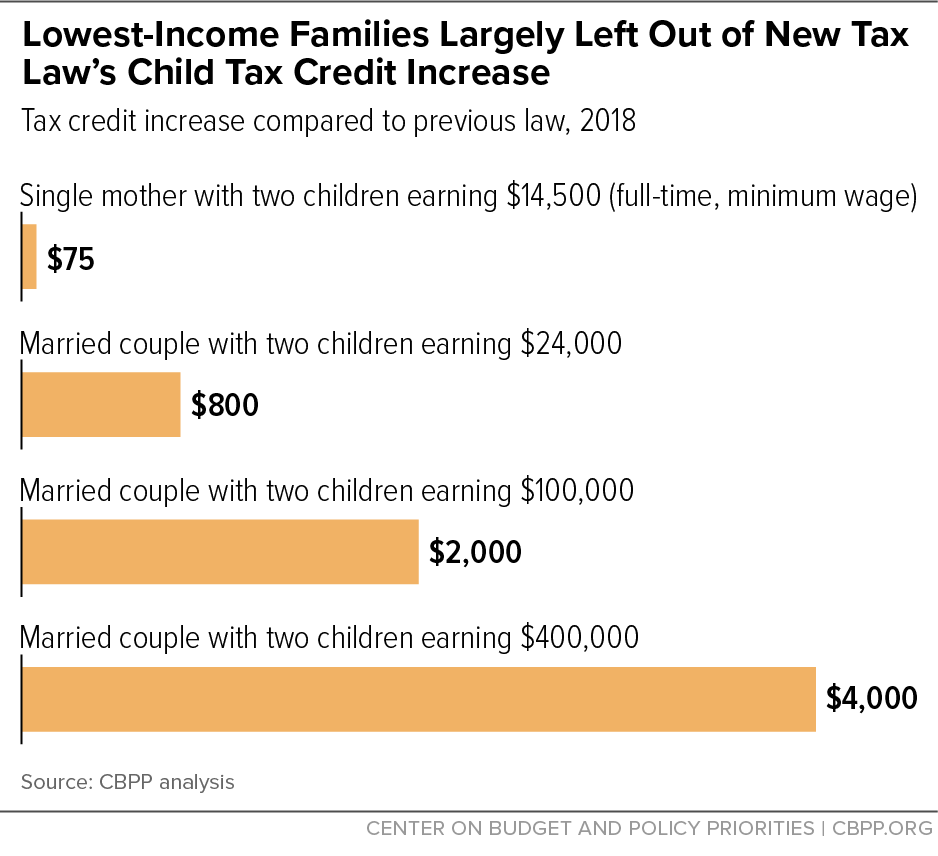

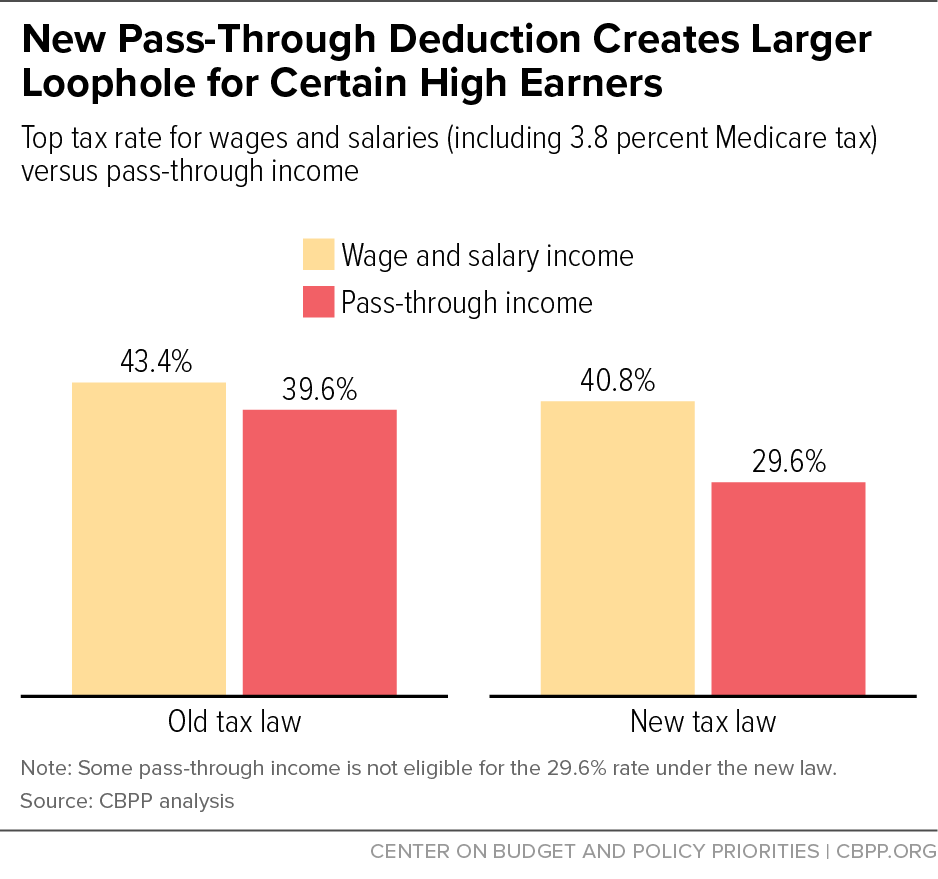

Last-minute decisions typified the bill’s skewed priorities. Negotiators lowered the top individual tax rate in the final bill to 37 percent — down from the Senate bill’s 38.5 percent and the House’s 39.6 percent — but rejected the effort by Senators Marco Rubio and Mike Lee to provide more than a token CTC increase for children in low-income working families. While Rubio and Lee secured a more adequate CTC increase for moderate-income families, 10 million children under age 17 in low-income working families will receive no CTC increase or a token increase of $75 or less.[15] Another 14 million children will get a CTC increase of more than $75 but less than the full $1,000-per-child increase that families with higher incomes will receive. Moreover, the law raises the income level at which the CTC begins phasing out from $110,000 to $400,000; as a result, a married couple with two children family making $400,000 will newly qualify for a $4,000 credit, while a single mother of two working full-time at the minimum wage will receive a $75 increase in her CTC. (See Figure 2.)

The new tax law not only shortchanges many working-class families but actually harms a number of them. Its repeal of the ACA’s individual mandate is expected to add millions to the ranks of the uninsured and raise premiums in the individual insurance market by about 10 percent, according to CBO.[16] This could also generate further instability in the individual health insurance market, especially in the near term, as falling enrollment, increased uncertainty, and growing confusion make it harder for insurers to forecast their costs.

The new tax law will also generate pressure to cut programs that millions of working- and middle-class families rely on. The $1-$2 trillion ten-year cost of the tax cuts adds to deficits initially but will have to be paid for at some point, through some combination of tax increases and spending cuts. In the end, it is likely that for millions of lower- and middle-income families, the budget cuts that the tax law will engender will reduce their incomes more than the tax cuts will increase them.

New Tax Law Ignores Critical Tool for Boosting Working-Class Incomes

Lawmakers drafting the new tax law appear not to have considered strengthening the Earned Income Tax Credit (EITC). Stagnant working-class wages call for a strong policy response, and the EITC is well-designed to be at the forefront of addressing this challenge. It already lifts millions out of poverty and supplements the wages of people who do needed jobs but receive relatively low pay, from truck drivers to cooks to home health aides. It is well placed to do more.

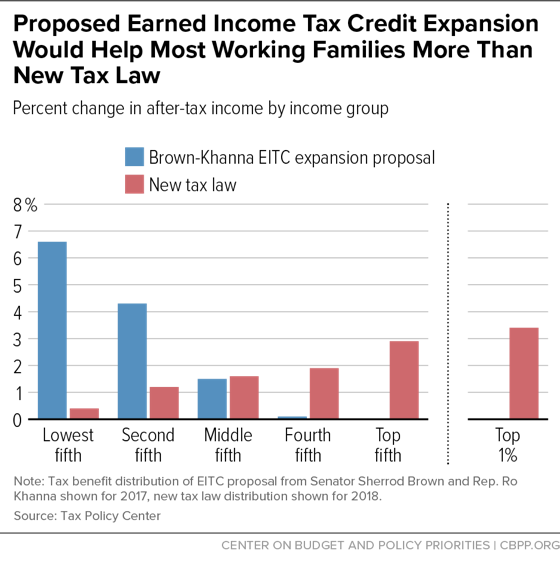

Ambitious EITC proposals are on the table. Senator Sherrod Brown and Rep. Ro Khanna, along with 55 House co-sponsors, have introduced a bill to substantially increase the EITC for childless workers and double it for workers with children, raising the incomes of 47 million households and lifting 8 million people out of poverty.a A median working-class family of three, which now makes $48,700, would receive a $2,800 EITC boost in 2018.b Such a proposal could have been paid for with progressive base-broadening measures. Those designing the new tax law also declined to make improvements to the small EITC for workers not raising minor children in their homes, thereby perpetrating features of the tax code under which more than 5 million such workers are literally taxed into — or deeper into — poverty by federal income and payroll taxes.c

This chart, which compares the effects of the new tax law and the Brown-Khanna proposal, underscores the law’s missed opportunity to address stagnant wages and growing inequality through such means as strengthening the EITC. Doing so should be part of future tax reform efforts to address the many problems that the new tax law creates.

a Chuck Marr, Emily Horton, and Brendan Duke, “Brown-Khanna Proposal to Expand EITC Would Raise Incomes of 47 Million Working Households,” CBPP, October 10, 2017, https://www.cbpp.org/research/federal-tax/brown-khanna-proposal-to-expand-eitc-would-raise-incomes-of-47-million-working.

b An alternative approach would have been a more ambitious CTC proposal. A bill introduced by Senators Michael Bennet (D-CO) and Brown would increase the maximum CTC to $3,000 per child ($3,600 per child under age 6), make the credit fully refundable, and pay it out on a monthly basis. Christopher Wimer and Sophie Collyer of Columbia University estimate that it would cut the child poverty rate nearly in half. See Christopher Wimer and Sophie Collyer, “Expanding the Child Tax Credit would Cut Child Poverty Nearly in Half,” Poverty and Social Brief 1 (3) (2017): https://static1.squarespace.com/static/5743308460b5e922a25a6dc7/t/59f0dab890bccea6185a078d/1508956859468/Poverty+and+Social+Policy+Brief_CTC__1_3.pdf.

c CBPP analysis of March 2017 Current Population Survey data.

We estimate that the new law’s $400 tax cut for the bottom 60 percent of households would turn into a $1,200 (2.8 percent) reduction in their after-tax incomes if each household ultimately pays an equal dollar amount each year in program cuts to pay for the tax cuts.[17] The actual impact could be worse: recent congressional Republican budgets have included large budget cuts that would fall harder, in dollar terms, on low- and moderate-income households than on more affluent ones. For example, those budgets have consistently featured large cuts in Medicaid, which provides health and nursing home care to millions of these families.

New Law Ignores Need for More Revenue

The new tax law costs $1.5 trillion over ten years (2018-2027), according to JCT, not counting its potential effects on the economy. This reflects the net effect of $1.6 trillion in revenue losses and $194 billion in spending cuts.[18]

JCT estimates that the new law could generate additional economic growth to offset a small share of this revenue loss, lowering the ten-year cost to roughly $1.1 trillion.[19] On the other hand, nearly all of the law’s changes to the individual income tax expire after 2025; extending them and other temporary provisions — as the plan’s supporters assert is their goal — would add more than $500 billion to its ten-year cost (and more than $250 billion annually by 2027).

Yet the nation is facing long-term fiscal challenges that will require more revenue, not less. The new law therefore weakens the tax system’s ability to deliver on its core responsibility: raising sufficient revenue to adequately finance critical national needs and avoid spiraling debt and interest burdens.

Major Cost Drivers Include Demographics, Health, and Interest Costs

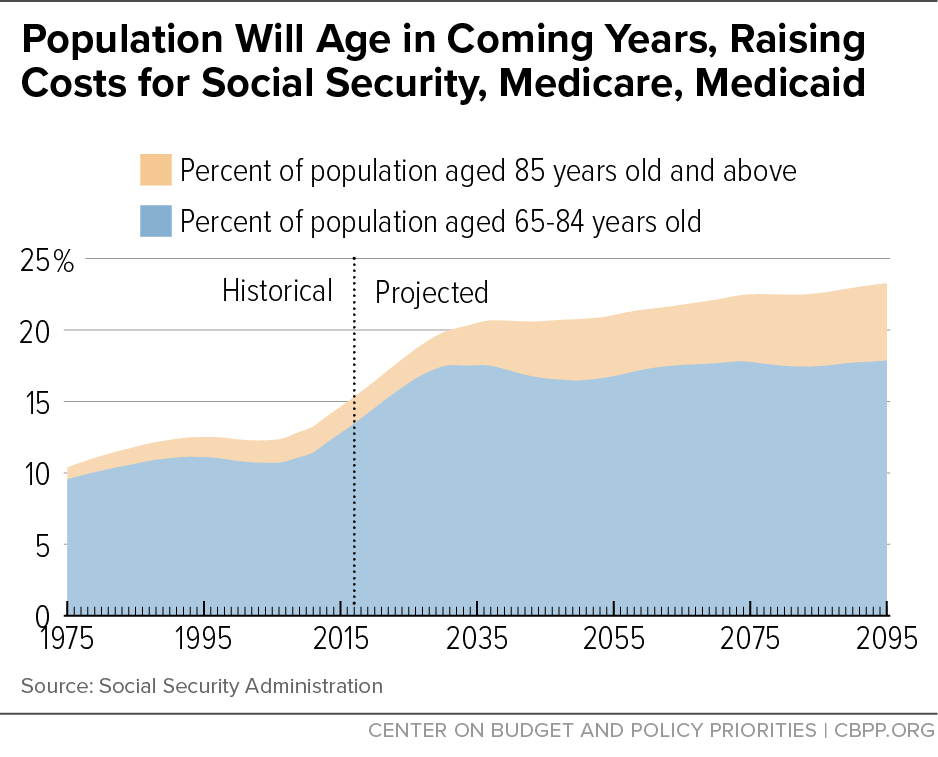

Federal spending will necessarily increase as a share of GDP over the next few decades due to several factors.[20] The most important is the aging of the population. For the next two decades, people 65 or older will grow from 15 percent to 21 percent of the population. And the “old-old” population — those over age 85, who have much higher health care costs than other elderly individuals — will grow even more rapidly. This will increase spending on programs such as Social Security, Medicare, and Medicaid.[21] (See Figure 3.)

Compounding the higher costs associated with these demographic realities, health care expenditures — in both the public and private sectors — have long grown faster than the economy and will likely continue to do so, in part due to new procedures, drugs, and treatments that improve health and save lives but also add to costs. In recent years, the pace of health care cost growth has slowed, but the extent to which the slowdown will persist is unknown.

Interest payments on the debt will also rise. Interest rates are expected to increase from their historically low levels to more normal levels; the Federal Reserve has begun gradually increasing interest rates, and most economic forecasters anticipate rates to continue rising in future years. The projected increase in the debt will raise interest payments further.

There also are strong pressures for higher spending outside Social Security and major health programs. Defense and non-defense discretionary programs have borne the bulk of deficit reduction efforts since 2010, and spending in both areas is well below their historical averages as shares of GDP. These reductions are not sustainable, as the recent bipartisan budget agreement that significantly boosts funding for these programs in 2018 and 2019 indicates. In addition, resources will surely be required — or demanded — to offset the cost of new federal initiatives to grapple with evolving challenges in the 21st century, such as the need to address a decaying infrastructure.

Policymakers should of course pursue appropriate avenues for achieving budgetary savings, such as eliminating duplicative, outdated, or ineffective programs and reducing errors and overpayments in federal programs. But the savings will not come close to offsetting the factors that will raise federal expenditures overall. Absent a radical shift in longstanding public values and preferences about the role of the federal government, more revenue will be needed.

Revenue Needs Will Grow Accordingly

Since 1976, federal spending has averaged 20.5 percent of GDP, although its composition has changed substantially, while federal revenue has averaged 17.4 percent of GDP. We estimate that federal spending will rise to roughly 23.5 percent of GDP in 2035 — an increase of 3 percentage points over the historical average — because of the factors noted above.[22] This projection is conservative; CBO projects spending will rise to 25.7 percent of GDP in 2035.[23]

Complicating this spending pressure, the debt stands today at 77 percent of GDP, high by historical standards, and is on a track to rise to over 100 percent of GDP over the next two decades.[24] While there are no absolute thresholds for when a debt-to-GDP ratio becomes problematic, a perpetually rising debt ratio is not sustainable over the long run, as it leaves less and less saving available for private investment. Stabilizing or reducing the debt-to-GDP ratio does not require balancing the budget or running surpluses; rather this sensible fiscal goal can be achieved as long as the debt is growing no more rapidly than the economy.

The foreseeable upward pressure on spending, combined with an already elevated debt-to-GDP ratio, means that policymakers will need to raise significant additional revenue over the next two decades. Revenues were 17.3 percent of GDP in 2017, or roughly at their 40-year average, before enactment of the tax-cut bill. To keep pace with the estimated growth in spending, revenues would need to rise by at least 3 percentage points of GDP by 2035, and possibly more.

The new tax law, however, does the opposite. Under it, revenues will fall below their historical average as a percent of GDP for the next several years, before beginning to edge up slowly. Indeed, as former Council of Economic Advisers Chair Jason Furman has pointed out, the only times that revenue has been so low as a percent of the economy in the past 50 years was in the aftermath of the past two recessions.[25]

The revenue picture later in the decade is less certain, because many of the new law’s provisions — particularly its changes to individual income taxes — are set to expire after 2025. (The bill’s drafters did this so that the bill would comply with Senate rules and could pass the Senate with a simple majority, rather than the 60 votes that would otherwise be required.) This means Congress will have a chance later in the decade to revisit these policies. But Congress should not wait that long; lawmakers should act as soon as possible to reverse the law’s fiscally irresponsible revenue losses and the upward pressure it is placing on deficits and debt.

New Law Risks Undermining Integrity of Tax Code

Well-designed tax reform eliminates loopholes and reduces opportunities for gaming the tax system so that individuals and businesses with the same income are treated as similarly as possible.[26] The new tax law moves in the opposite direction.

Narrowing the gaps between how different types of income are taxed brings several benefits. First, it increases the degree to which individuals and businesses base their decisions on economics instead of taxes. This is good for the economy: it encourages resources such as capital and labor to flow to where they are most productive instead of where the tax breaks and gaming opportunities are most plentiful. Second, it reduces the amount of economic resources that are diverted to developing sophisticated tax avoidance schemes that provide little overall economic benefit, allowing those resources to go to more productive uses. Third, closing loopholes and eliminating opportunities for gaming raises revenue and may also reduce inequality, since wealthy individuals and corporations are best equipped to exploit these weaknesses in the tax code.

The tax code previously had plenty of distortions that invited tax gaming, but the new law creates new gaming opportunities.[27] In particular, its 20 percent pass-through deduction and deep cut in the corporate tax rate to 21 percent risk making the 37 percent top individual tax rate merely theoretical for some very wealthy people. The new law also confers enormous tax benefits on some industries but not others, makes it easier for wealthy households to shelter their assets and thereby accumulate multi-million-dollar fortunes, and favors business production and investment overseas rather than at home. Widespread abuse and gaming of the bill’s loopholes and preferences could cause it to lose revenue and increase inequality even more than current projections indicate.

Pass-Through Provision Invites Abuse

The core of the new tax law is a deep cut in the corporate tax rate. Many businesses are organized as pass-through entities, however, and do not pay the corporate tax, so lawmakers were under political pressure to provide a tax cut for pass-throughs as well.

Yet while adding a pass-through tax cut to the bill may have made sense politically for those crafting this legislation, it never enjoyed a solid policy rationale. Although proponents argued that it was necessary to maintain “parity” between the two types of business taxes, pass-throughs already enjoyed a tax advantage over regular corporations (known in the tax code as C corporations) under prior law, as research demonstrated.[28] That’s one reason why the number of pass-throughs has grown so dramatically in recent years. While pass-through income faces only one layer of taxation — at the individual level — C corporation income faces two levels of tax: one when the firm pays the corporate income tax, and another when shareholders pay individual income tax on their dividends or capital gains.

Efforts to help pass-through businesses also ignored the fact that they will benefit from other provisions of the new tax law not aimed specifically at them, such as the law’s income-tax rate cuts. Further, pass-throughs can always convert to a C corporation if that would be advantageous to them. As tax expert Michael Schler has noted, under the new tax law, “by merely checking a box on a tax form, a passthrough business can elect, on a tax-free basis, to be a C corporation and obtain” the new 21 percent corporate tax rate.[29]

Nevertheless, the drafters of the new law included in it a 20 percent deduction for pass-through income. As noted above, this provision is tilted to wealthy business owners, who receive a very large share of existing pass-through income. It also creates a significant gaming opportunity: many high-income individuals may now be able to secure very large tax savings by converting their wage and salary income into pass-through income to take advantage of the new deduction.

To be sure, the law includes a series of complex “guardrails” aimed at limiting the scope of the provision and preventing gaming, but these measures are unlikely to be effective. They consist of a series of questions for taxpayers to determine whether particular income qualifies for the pass-through deduction, with each question drawing a line between qualification and disqualification for the deduction. This will entice many taxpayers, aided by their accountants or lawyers, to try to place themselves on the tax-saving side of each line.[30]

One such line is between compensation and profits for S corporations (a type of pass-through business that has a maximum of 100 owners and whose profits are taxed on the owners’ individual returns).[31] The law, in effect, asks S corporation owners whether the income in question is compensation (in which case the deduction is not allowed) or profit (in which case it is allowed). This distinction has existed in the tax code for many years, however, and it hasn’t been particularly effective at stopping taxpayers from recharacterizing compensation as profit to obtain tax savings, even when the potential savings from doing so were much smaller than they will be under the new law.

For instance, many S corporation owners receive both wages from the S corporation and a share of the S corporation’s profits, but they pay payroll tax only on their wages. Even before the new tax law, this gave them an incentive to underreport the share of their income that consists of wages or salaries (compensation) and overstate the share that is due to profits, in order to shrink their payroll tax liability.[32] Under prior law, however, S-corporation earners could reduce their tax rate by only 3.8 percentage points (reflecting the Medicare payroll tax that high earners pay) through this maneuver, since pass-through income was otherwise taxed at the same rates as wages and salaries. Under the new law, by contrast, the tax-rate differential between wage and salary income and pass-through income that is eligible for the 20 percent deduction is more than twice as large for high earners: 11.2 percentage points.[33] (See Figure 4.) Thus, these taxpayers now have a much greater incentive to recharacterize wage and salary income as pass-through profit income.

The new law draws another line by denying the new pass-through deduction to high-income individuals in certain “personal services” industries, such as medicine, law, accounting, consulting, financial services, and athletics. [34] And it draws another line for high-income individuals who do qualify for the deduction by basing the size of their pass-through deduction on the amount of wages the firm pays or the value of the property it owns — the larger the overall amount of wages and salaries the firm pays or the greater the value of the property it owns, the larger the amount that the firm’s owners can deduct via the pass-through deduction. In an earlier version of the bill, the deduction was only based on the amount of a firm’s wages and salaries, in order to prevent firms with few if any employees from receiving large pass-through deductions. But late in the legislative process, the bill’s drafters opened a large escape-valve from that requirement by also allowing a firm to base the amount of its deduction on the value of its property. This change especially benefits asset-heavy industries such as real estate, which will be able to take large deductions based on the property they own even if they have few employees. (The real estate industry also benefits from the fact that one kind of real estate structure, Real Estate Investment Trusts or REITs, qualifies for the pass-through deduction automatically.)

The new law thus gives taxpayers who find themselves on the “wrong” side of one of these lines a strong incentive to get to the other side. A group of 13 leading tax experts have highlighted potential tactics of “cracking” and “packing”— that is, splitting apart different aspects of a business, or combining different businesses together, in ways that maximize the new tax break. For example, a group of doctors could form a REIT and purchase their medical practice’s building.[35] The REIT would “charge” the medical practice “rent” to use the building, and the rental income that the doctors essentially paid themselves would become eligible for the pass-through deduction (REIT income is eligible for the deduction). Moreover, the highly paid doctors would have an incentive for their REIT to overcharge the medical practice for rent, effectively shifting income from a form that isn’t eligible for the deduction (their medical practice income) to one that is eligible (their REIT income).

Beyond inviting abuse, the arbitrariness of the pass-through provision undermines the integrity of the entire income tax. For instance, a last-minute change to the tax bill excluded architects and engineers from the list of “professional services” that cannot receive the deduction. The law’s drafters provided no policy rationale for this last-minute change; rather, these industry-based exclusions appear simply to pick winners and losers.

Features such as these bolster NYU law professor Daniel Shaviro’s damning description of the pass-through provision as “the worst provision ever even to be seriously proposed in the history of the federal income tax.”[36]

Deep Cut in Corporate Rate Risks Encouraging Tax Sheltering

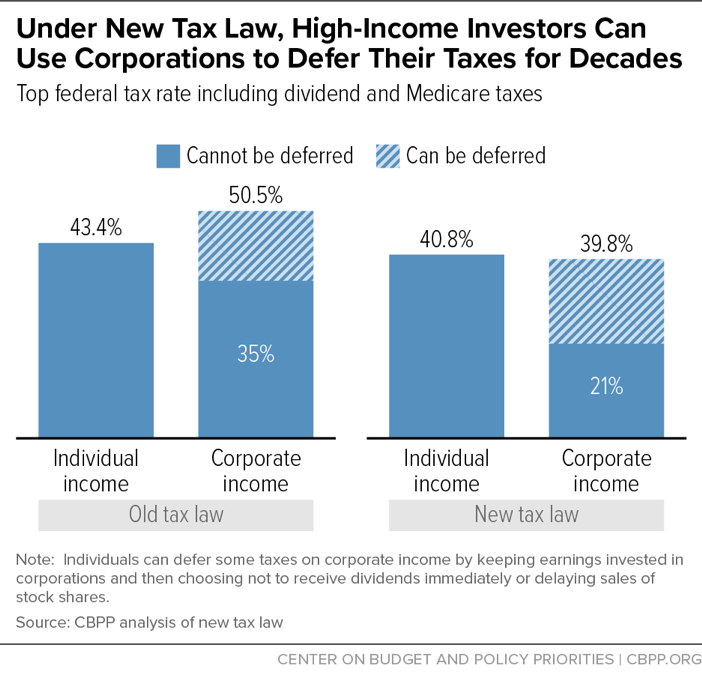

The new law’s cut in the corporate tax rate to 21 percent will not only primarily help the wealthiest Americans, as explained above, but may also turn C corporations into a potential tax sheltering device. Under prior law, income subject to the top individual tax rate faced lower taxes than corporate income: the top individual rate was effectively 43.4 percent (the 39.6 percent individual income tax plus a 3.8 percent Medicare payroll tax), while corporate profits faced a combined tax rate of 50.5 percent (a top rate of 35 percent on corporate earnings, plus a second level of tax at the individual level for dividends or capital gains[37]). Thus, wealthy individuals had no significant tax incentive to use a C corporation as a tax shelter.

The new law changes this dynamic. The tax rates on ordinary income and C-corporation income are now similar: the new top individual rate is effectively 40.8 percent (the new 37 percent top individual income tax rate plus the 3.8 percent Medicare payroll tax rate), while the combined rate on C corporation income is 39.8 percent (the top corporate rate of 21 percent plus the second layer of individual taxes).[38] But high earners and wealthy investors can defer the second level of tax, such as by electing not to receive dividends immediately or by delaying selling shares and realizing a capital gain. They cannot defer any of the tax on ordinary income. (See Figure 5.)

The deferral of this second layer of tax means that under the new law, invested earnings sheltered inside a C corporation can compound and grow much more quickly than ordinary income, since they can face only the 21 percent corporate tax each year, instead of the 40.8 percent rate under the individual income tax. Thus, high earners may be able to shield their labor income from the top individual rate by setting up a corporation and reclassifying their income as corporate profits.[39] As tax expert Michael Schler has pointed out, investors may be able to do the same with bonds since bond interest is taxed as ordinary income.[40]

Moreover, as NYU tax law professor David Kamin and his colleagues have noted, “pre-existing safeguards to avoid these kinds of consequences are already inadequate and will be even more so in light of the planning incentives that this [new] rate differential creates.”[41] It is troubling that the drafters of the law did nothing to prevent abuse of this rather obvious sheltering opportunity.

Deferring this second layer of tax could be especially lucrative since wealthy Americans have various avenues to avoid that tax altogether, as Adam Looney of the Brookings Institution has shown.[42] For instance, wealthy households can hold their shares of a C corporation that’s being used as a tax shelter in a Roth Individual Retirement Account (IRA), which allows distributions to be made in retirement tax-free.[43] (While they would have to pay taxes up front on the earnings deposited into the Roth IRA that then are used to purchase or establish the corporation, they would pay only the 21 percent corporate tax on the earnings that subsequently accrue inside this shelter.)

The new tax law also encourages income sheltering by retaining the “stepped-up basis” loophole, which allows the heirs of an estate not to pay any taxes on any appreciation of an asset that occurred during the previous owner’s lifetime. For example, if a share of stock that someone bought for $10 when they were young is worth $110 when they die, the person inheriting the stock owes no capital gains tax on that $100 gain.

Thus, if a wealthy investor keeps his or her bond portfolio and its earnings inside the C corporation being used as a tax shelter and retains ownership of the corporation until his or her death, the entire second level of tax on the capital gains over the investor’s lifetime will be wiped out. The bond income will only be taxed at the initial 21 percent corporate tax rate, far below the 40.8 percent rate it would have faced outside the shelter. Combined with the new law’s doubling of the estate-tax exemption level, this will substantially increase the amount of income that can go entirely untaxed by enabling wealthy people to shelter more income from tax during their lifetimes and then pass it along tax-free to their heirs.[44]

New International Tax Regime Encourages Offshoring and Profit Shifting

The new tax law moves the U.S. international tax system to a “territorial” system, where most profits that a U.S. parent company earns from its foreign subsidiaries aren’t subject to U.S. tax if they meet certain conditions. This system risks creating a large, permanent incentive for U.S. multinationals to shift overseas not just profits on paper but actual investment as well. This could lead to a reduction in capital investment in the United States and thereby wind up reducing U.S. workers’ wages, as Congressional Research Service economist Jane Gravelle has explained.[45]

The law includes several provisions to try to limit the damage this incentive could cause, but they don’t alter the basic incentive to shift profits and investment offshore. For example, a central anti-abuse measure in the new law — a new minimum tax on certain foreign income — is poorly designed and may actually increase incentives for companies to shift profits and investments overseas.

The minimum tax is supposed to ensure that U.S. companies pay a U.S. tax on foreign profits when the foreign taxes on those profits are sufficiently low. The tax applies to annual foreign income that exceeds 10 percent of the value of the firm’s tangible assets (such as factories) in foreign countries. The idea is that a company’s tangible assets should yield a “routine” rate of return of 10 percent, so any income above that exemption amount must arise from intangible assets (typically intellectual property such as patents, copyrights, and trademarks).[46] This structure, however, creates several problems.

First, the exemption amount is well above a “routine” rate of return for tangible assets, given that 10 percent is considerably higher than the historical average rate of return on low-risk or risk-free investments.[47] This allows a high level of foreign profits that face little or no tax overseas to completely avoid U.S. tax. Moreover, since the amount of a company’s foreign income that’s entirely exempt from U.S. tax will equal 10 percent of the firm’s tangible assets abroad, companies will have an incentive to increase their foreign tangible assets, since the greater such assets abroad are, the more foreign income a company can shield from the minimum tax. Indeed, a firm with sufficient tangible assets abroad can face no U.S. tax whatsoever on its foreign profits even if the firm pays minimal foreign taxes as well.

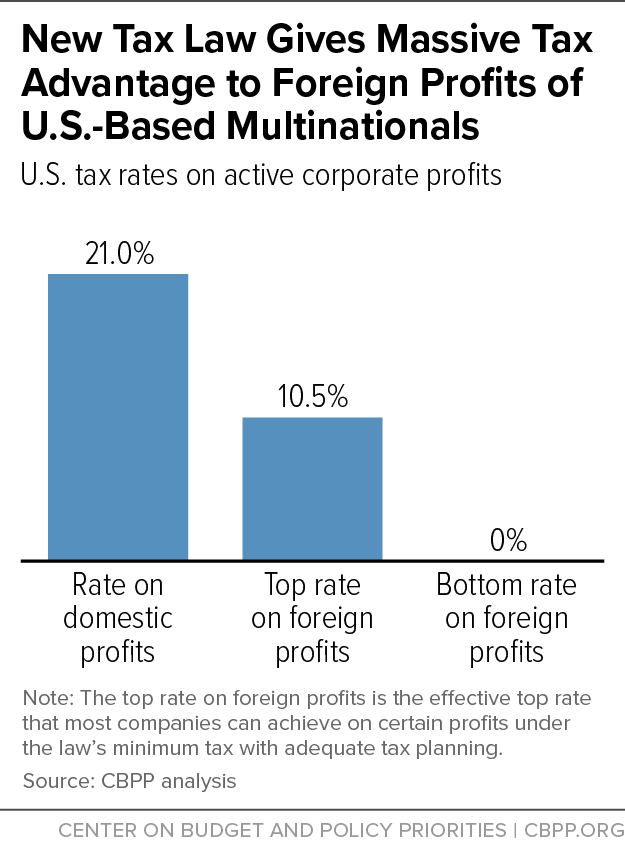

Second, foreign income subject to the new U.S. minimum tax receives a 50 percent deduction off the normal 21 percent corporate rate, so income above the exemption level is effectively only taxed at a 10.5 percent U.S tax rate.[48] Combined with the generous exemption level, this means that foreign income could easily face an effective tax rate in the single digits — well below the 21 percent rate on domestic profits. (See Figure 6.)

Third, the minimum tax is based on a multinational’s global income and non-U.S. taxes, instead of its income and taxes for each country separately.[49] If the new law had required that countries be treated separately, then profits from tax havens (where companies typically have little or no tangible assets) would have been eligible for little or no exemption. But by allowing all foreign income to be aggregated, the new law further encourages companies to shift some profits to tax havens and combine them with profits earned from real economic activity (such as manufacturing or sales) in higher-tax countries. Blending together the taxes and income from both sets of countries will allow multinational corporations to secure a global tax rate that is as low as possible, and possibly to avoid the U.S. minimum tax altogether.[50] The taxes that a company pays on profits from a retail outlet in Italy can thus shield from the U.S. minimum tax the profits it reports in tax havens like Bermuda (where it faces no corporate tax). Indeed, in some cases this may create an incentive for companies to invest in countries with tax rates similar to or greater than those in the United States, since income earned in those countries can be used to help tax-haven profits escape the minimum tax.

For all of these reasons, the new tax law may lead a number of multinational corporations to shift investments out of the United States to foreign countries. (See the Appendix for a further discussion of this issue.)

Recognizing that even with its minimum tax, the new law will create tax incentives for companies to locate intangible assets overseas, the law includes another provision to encourage companies to keep them in the United States: it taxes certain income that arises from exports at a lower rate (13.125 percent[51]) than income from domestic profits (21 percent).[52] Yet this provision brings its own risk of gaming. A U.S. company, rather than sell a product in the United States and pay a 21 percent tax on the profits, may be able to “export” the product by selling it to a foreign distributor, which can then sell the product back in the United States. The profits from this “export” would then be taxed at a 13.125 percent rate, even though a U.S. company created the product and U.S. consumers purchased it. According to tax expert Michael Schler, to avoid substantial gaming, “elaborate regulations will be required to show how a taxpayer can establish that goods are sold for foreign use and will not be resold back into the United States.”[53] There is no guarantee that effective regulations will be developed, issued, and enforced.

Beyond the major risk of gaming, this provision could violate World Trade Organization (WTO) rules. Brooklyn University Law professor Rebecca Kysar and University of Michigan law professor Reuven Avi-Yonah have concluded that the lower rate on exports is a type of trade subsidy that the WTO’s Subsidies and Countervailing Measures Agreement explicitly bans.[54] The European Union is already raising WTO concerns with the Treasury over this provision,[55] and these legal challenges may render this provision even less effective.[56] Overall, it likely will do little to reduce the risk that the flaws in the minimum tax will encourage companies to shift profits and production to foreign countries.

In sum, the new tax law’s changes to the international tax system create incentives for companies to move profits, investment, and jobs overseas, and the provisions it offers to stem abuse are likely to be largely ineffective (and potentially create other perverse incentives). Ironically, the proposal that then-candidate Donald Trump made during the campaign — to immediately tax profits made from overseas investments just like profits from domestic investments are taxed — would have avoided these problems. Instead, President Trump dropped his proposal and joined congressional Republicans in pushing for a territorial system, which features tax-free foreign profits and a major tilt in favor of overseas investment, along with anti-abuse measures to limit the damage that are likely to be of limited effectiveness.

Conclusion

Much of the discussion over the new tax law has moved from its design to its implementation. The Treasury Department has begun developing regulations to clarify the law, while the Internal Revenue Service (IRS) must prepare to implement and enforce it (the IRS will need a significant and sustained increase in funding to do this properly,[57] but Congress has provided inadequate funding).[58] Such efforts, however, cannot overcome the law’s fundamental flaws. Only a basic restructuring of the law can fix these flaws, as they stem from the law’s core provisions.

The corporate rate cut and the 20 percent deduction for pass-through businesses, in particular, contribute to all three of the measure’s major flaws: they worsen inequality by disproportionately benefiting the well-off; they lose significant revenue at a time when demographic and other pressures require federal revenue to rise; and they will likely encourage significant tax avoidance by creating major incentives for wealthy individuals to recharacterize their income in search of lower taxes. Minor tinkering or technical corrections cannot solve these problems.

Policymakers should begin considering ways to reverse the damage the new law is expected to cause and to craft meaningful tax reform that eliminates various loopholes, shelters, and gaming opportunities the tax code now contains, raises much-needed revenue, and is more favorable to working households with low or modest incomes.

Appendix

How New Tax Law Encourages Overseas Investment: An Example

The following stylized example illustrates how the new tax law’s international provisions can encourage companies to shift not just profits overseas, but actual investment and jobs as well. Imagine a U.S. company that earns $500 million per year in pre-tax profits and has $3 billion in tangible assets (such as manufacturing plants), all in the United States. The $500 million in profits reflects the return on both the company’s tangible assets and its intangible assets, such as its intellectual property (e.g., patents and trademarks). Under the new tax law, the company will pay $105 million in U.S. corporate taxes ($500 million in profits multiplied by 21 percent). The company’s global effective tax rate is 21 percent.

To reduce its taxes, the company could shift $300 million in profits to a tax haven with no corporate tax. This shift does not reflect any actual economic activity — the firm could set up a foreign subsidiary that acquires the company’s intellectual property (i.e., its intangible assets) and thereby garners $300 million of the annual profits.[59] (Assume in this stylized example that the relocation of the firm’s intangible assets passes muster with the IRS.[60])

Since the company has no tangible foreign assets, none of its foreign income qualifies for an exemption from the minimum tax. But it is eligible for the 50 percent deduction that the new law provides on a firm’s foreign profits, which lowers the taxable amount from $300 million to $150 million. [61] As a result, the company now owes a tax of just $31.5 million ($150 million in taxable profits multiplied by the 21 percent rate) on its foreign profits, plus another $42 million in U.S. tax on its $200 million in profits that remain in the United States. By shifting some of its income overseas, the company has reduced its tax bill from $105 million to $73.5 million, and its global effective tax rate from 21 percent to 14.7 percent.

In addition, through a series of complicated transactions, the company could further reduce its global tax bill by shifting its remaining U.S. profits to another subsidiary in a different foreign country, even one with a higher corporate tax rate than the United States. Assume, for instance, that the company moves all of its $3 billion in tangible assets — and with that move, its remaining $200 million in pre-tax profits — to a country with a 25 percent corporate tax rate. In this way, the company can lower its global tax bill to $54.2 million ($50 million to the higher-tax country, plus $4.2 million to the United States, as explained below) and its global effective tax rate from 14.7 percent to 10.8 percent.

Here are the calculations to determine the company’s $4.2 million in U.S. taxes:

- Having shifted all of its tangible and intangible assets overseas, the company no longer generates U.S. profits and so would not face the U.S. corporate tax on U.S. profits (as distinguished from the U.S. minimum corporate tax it would owe on its foreign profits).

- The company pays no foreign taxes on the $300 million in profits generated by its intangible assets located in an overseas tax haven, but it pays $50 million in taxes on the $200 million in profits that it earns from its tangible assets in the higher-tax country ($200 million in profits multiplied by that country’s 25 percent rate). This $50 million in foreign taxes reduces the firm’s foreign profits potentially subject to U.S. minimum tax to $450 million.

- The firm’s U.S. minimum tax is calculated by aggregating the income and assets of the company’s two foreign subsidiaries. Since the company’s foreign subsidiaries hold $3 billion in tangible foreign assets, 10 percent of the value of those assets — or $300 million in profits — is exempt from the minimum tax. This leaves $150 million of its $450 million in remaining foreign profits — one-third of them — potentially subject to the U.S. minimum tax.

- Next, because one-third of the firm’s remaining foreign profits (the $150 million just noted) could face the U.S. minimum tax, one-third of the $50 million that the firm paid in foreign taxes — or $16.7 million — is added back to the $150 million. The resulting total of $166.7 million then qualifies for the 50 percent deduction noted above that applies to a firm’s otherwise-taxable foreign profits. This results in the firm having net income subject to the U.S. minimum tax of $83.3 million. The tentative minimum tax on this amount is $17.5 million ($83.3 million multiplied by 21 percent).

Under the new minimum tax system, however, companies also receive a tax credit equal to 80 percent of the foreign taxes they pay on the share of their overseas profits that face the U.S. minimum tax (subject to a possible further limitation[62]). As noted in the second bullet above, the company pays $50 million in foreign taxes. And as noted in the third bullet above, only one-third of the company’s foreign profits are subject to the U.S. minimum tax. As a result, this tax credit is worth $13.3 million — 80 percent times 33.3 percent times the $50 million that the company pays in foreign taxes. This $13.3 million credit further reduces the minimum tax that the company owes — from $17.5 million to $4.2 million.

End Notes

[1] The law’s official name is “Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018.” It was originally titled the “Tax Cuts and Jobs Act” (TCJA) but that name was stricken from the bill.

[2] The authors thank Professor David Kamin for helpful comments. The authors remain responsible for any errors.

[3] Howard Gleckman, “The Downmarketing of Tax Shelters,” TaxVox, January 18, 2018.

[4] Tax Policy Center Table T17-0314, http://www.taxpolicycenter.org/model-estimates/conference-agreement-tax-cuts-and-jobs-act-dec-2017/t17-0314-conference-agreement.

[5] The share of income going to the top 1 percent increased from 7.4 to 13.1 percent, while the share going to the bottom 60 percent fell from 36.3 to 31.9 percent. Congressional Budget Office, “The Distribution of Household Income, 2014,” March 19, 2018, https://www.cbo.gov/publication/53597. Income shares have been recalculated to exclude households with negative income.

[6] Chuck Marr, Brandon DeBot, and Emily Horton, “How Tax Reform Can Raise Working-Class Incomes,” CBPP, updated October 13, 2017, https://www.cbpp.org/research/federal-tax/how-tax-reform-can-raise-working-class-incomes.

[7] Some provisions of the new law raise taxes on high-income households, such as its limit on the deduction for state and local taxes (SALT), but the progressive provisions are overwhelmed by the regressive ones, resulting in a highly regressive law overall, as TPC analyses show.

[8] Chye-Ching Huang and Brandon DeBot, “Corporate Tax Cuts Skew to Shareholders and CEOs, Not Workers as Administration Claims,” CBPP, updated August 16, 2017, https://www.cbpp.org/research/federal-tax/corporate-tax-cuts-skew-to-shareholders-and-ceos-not-workers-as-administration.

[9] Chye-Ching Huang, “Senate’s ‘Pass-Through’ Tax Cut Favors Biggest Businesses and Wealthiest Owners,” CBPP, November 14, 2017, https://www.cbpp.org/blog/senates-pass-through-tax-cut-favors-biggest-businesses-and-wealthiest-owners.

[10] Christopher R. Tamborini, ChangHwan Kim, and Arthur Sakamoto, “Education and Lifetime Earnings in the United States,” Demography, 52 (4) (2015): 1383-1407.

[11] Chuck Marr, Brandon DeBot, and Chye-Ching Huang, “Eliminating Estate Tax on Inherited Wealth Would Increase Deficits and Inequality,” CBPP, updated April 13, 2015, https://www.cbpp.org/research/federal-tax/eliminating-estate-tax-on-inherited-wealth-would-increase-deficits-and.

[12] David Joulfaian, “Inheritance and Saving,” National Bureau of Economic Research Working Paper No. 12569, 2006, http://www.nber.org/papers/w12569.pdf.

[13] This calculation only counts the effect of reducing the top rate from 39.6 percent to 37 percent; it does not include the additional tax cut resulting from the top rate beginning at $600,000 instead of $480,050 as under previous law.

[14] TPC Table T17-0317

[15] Chye-Ching Huang, “Final CTC Changes Don’t Alter Tax Bill Basics: 10 Million Working Family Children Get Little or Nothing,” CBPP, December 15, 2017, https://www.cbpp.org/blog/final-ctc-changes-dont-alter-tax-bill-basics-10-million-working-family-children-get-little-or.

[16] Aviva Aron-Dine, “Senate Tax Bill Would Add 13 Million to Uninsured to Pay for Tax Cuts of Nearly $100,000 Per Year for the Top 0.1 Percent,” CBPP, November 15, 2017, https://www.cbpp.org/blog/senate-tax-bill-would-add-13-million-to-uninsured-to-pay-for-tax-cuts-of-nearly-100000-per-year.

[17] Our methodology is the same as in William G. Gale, “Who Would Pay For The Tax Cuts and Jobs Act?,” Tax Policy Center, December 8, 2017, http://www.taxpolicycenter.org/taxvox/who-would-pay-tax-cuts-and-jobs-act.

[18] After including the interest on the additional debt that the new law will create, the cost comes to $1.8 trillion over ten years. Congressional Budget Office, “Cost Estimate for the Conference Agreement on H.R. 1,” December 15, 2017, https://www.cbo.gov/publication/53415.

[19] Other credible, mainstream organizations such as the Penn-Wharton Budget Model and TPC, reached similar conclusions. See Joel Friedman and Chad Stone, “Republican Tax Plans Cost More — and Add Less to Growth — Than Proponents Claim,” CBPP, December 14, 2017, https://www.cbpp.org/research/federal-tax/republican-tax-plans-cost-more-and-add-less-to-growth-than-proponents-claim.

[20] For a thorough discussion of these factors, see Paul N. Van de Water, “Federal Spending and Revenues Will Need to Grow in Coming Years, Not Shrink,” CBPP, September 6, 2017, https://www.cbpp.org/research/federal-budget/federal-spending-and-revenues-will-need-to-grow-in-coming-years-not-shrink.

[21] In contrast, mandatory (entitlement) spending outside of Social Security and health care is already below average in historical terms, measured as a share of GDP, and is projected to fall still further. This diverse set of programs includes safety net programs such as SNAP (food stamps), Supplemental Security Income for the elderly and disabled poor, unemployment insurance, and the refundable parts of the Earned Income Tax Credit and Child Tax Credit. For more, see Van de Water 2017.

[22] Van de Water, 2017.

[23] Congressional Budget Office, “The 2017 Long-Term Budget Outlook,” March 30, 2017, https://www.cbo.gov/publication/52480.

[24] Ibid.

[25] Dylan Matthews, “Obama’s chief economist: Trump’s economic projections are ‘the most absurd I’ve ever seen,’” Vox, February 19, 2018, https://www.vox.com/policy-and-politics/2018/2/19/17012288/trump-budget-proposal-obama-chief-economist-jason-furman-interview.

[26] It may be appropriate to tax income differently to address “externalities,” where the income generated by an economic activity does not fully reflect the social costs or benefits of the activity. For example, scientific research can have positive externalities while pollution causes negative externalities. In these cases, the tax code may attempt to correct for the externality by taxing activity with positive externalities more lightly (e.g., through the research and development tax credit) and taxing behavior with negative externalities more heavily (e.g., via a carbon tax).

[27] See, for example, Chuck Marr, Chye-Ching Huang, and Joel Friedman, “Tax Expenditure Reform: An Essential Ingredient of Needed Deficit Reduction,” CBPP, February 28, 2013, https://www.cbpp.org/research/tax-expenditure-reform-an-essential-ingredient-of-needed-deficit-reduction?

[28] Congressional Budget Office, “Taxing Capital Income: Effective Marginal Tax Rates Under 2014 Law and Selected Policy Options,” December 18, 2014, https://www.cbo.gov/publication/49817; Michael Cooper et al., “Business in the United States: Who Owns it and How Much Tax Do They Pay?,” in Tax Policy and the Economy, ed. Jeffrey R. Brown National Bureau of Economic Research, 2016, Vol. 30.

[29] Michael Schler, “Reflections on the Pending Tax Cuts and Jobs Act,” Tax Notes, December 18, 2017, pp. 1731-1732.

[30] For a visual representation of these lines, see Latham & Watkins, “US Tax Reform: Key Business Impacts, Illustrated With Charts and Transactional Diagrams,” January 10, 2018, https://m.lw.com/thoughtLeadership/US-tax-reform-key-business-impacts-charts-transactional-diagrams.

[31] This issue goes beyond S corporations, as the law seems to apply this “reasonable compensation” test to “any” qualified trade or business. For more, see David Kamin, “Uncertainty, Perverse Incentives, and More,” Medium, January 11, 2018, https://medium.com/whatever-source-derived/uncertainty-perverse-incentives-and-more-a7af2d143a70.

[32] Matthew Smith et al., “Capitalists in the Twenty-First Century,” July 23, 2017, https://eml.berkeley.edu/~yagan/Capitalists.pdf.

[33] Wage and salary income previously faced a top marginal tax rate of 43.4 percent (39.6 percent in ordinary income tax + 3.8 percent in Medicare taxes), while pass-through profits faced a top tax rate of 39.6 percent, a differential of 3.8 percentage points. Under the new law, wage and salary income faces a top marginal tax rate of 40.8 percent (37 percent in ordinary income tax + 3.8 percent in Medicare taxes), while pass-through profits eligible for the deduction face a top rate of just 29.6 percent (37 percent x 80 percent because of the 20 percent deduction). The differential between the top rates on wage and salary income and pass-through profits eligible for the deduction thus is now 11.2 percent (40.8 percent versus 29.6 percent).

[34] The restrictions based on profession and wages/property only apply to married couples with taxable income over $315,000 and singles with taxable income over $157,500.

[35] David Kamin et al., “The Games They Will Play: An Update on the Conference Committee Tax Bill,” December 18, 2017, https://ssrn.com/abstract=3089423.

[36] Daniel Shaviro, “Apparently income isn’t just income any more,” Start Making Sense, December 16, 2017, http://danshaviro.blogspot.com/2017/12/apparently-income-isnt-just-income-any.html.

[37] Specifically, the 50.5 percent tax rate on corporate income for wealthy individuals consisted of a 35 percent corporate tax on profits plus a 23.8 percent tax on the profits remaining after the corporate income tax is paid; the 23.8 percent tax reflects a 20 percent tax on dividends and capital gains plus the 3.8 percent Net Investment Income Tax on high-income individuals enacted as part of the Affordable Care Act ($100 x 35 percent = $35; $65 x 23.8 percent = $15.5; and $35 + $15.5 = $50.5).

[38] Under the new law, the 39.8 percent tax consists of a 21 percent tax on corporate profits and the same 23.8 percent tax on remaining profits ($100 x 21 percent = $21; $79 x 23.8 percent = $18.8; and $21 + $18.8 = $39.8).

[39] Kamin et al. 2018 dub this the “You, Inc. strategy.”

[40] Schler 2017, p. 1733.

[41] Kamin et al., p. 4.

[42] Adam Looney, “The next tax shelter for wealthy Americans: C-corporations,” Brookings Institution, November 30, 2017, https://www.brookings.edu/blog/up-front/2017/11/30/the-next-tax-shelter-for-wealthy-americans-c-corporations/.

[43] Ibid.; Kamin et al. 2017, p. 7.

[44] See, for example, Looney and Kamin et al.

[45] Jane Gravelle, “The Need for Comprehensive Tax Reform to Help American Companies Compete in The Global Market And Create Jobs for American Workers,” House Ways and Means Committee hearing, May 12, 2011, https://www.gpo.gov/fdsys/pkg/CHRG-112hhrg70882/html/CHRG-112hhrg70882.htm.

[46] The new tax law refers to this as “Global Intangible Low-Taxed Income” or “GILTI.”

[47] The interest rate on a ten-year Treasury bond in April of 2018, for example, was about 2.8 percent.

[48] Like much of the rest of the bill, the deduction is slated to fall from 50 percent to 37.5 percent after 2025 and the rate will correspondingly rise to 13.125 percent.

[49] Similar to previous law, companies also receive a credit on the foreign taxes they do pay. This credit amounts to 80 percent of foreign taxes — a firm paying $100 in foreign taxes can thus reduce its U.S. minimum tax by $80.

[50] Rebecca M. Kysar, “The G.O.P.’s 20th-Century Tax Plan,” New York Times, November 15, 2017, https://www.nytimes.com/2017/11/15/opinion/republican-tax-plan-economy.html.

[51] The rate rises to 16.406 percent in 2026.

[52] The lower rate is intended to apply to export income derived from intangible sources. Like the minimum tax, this provision defines “intangible export income” to be income above 10 percent of the value of the tangible assets used to generate the export income. Schler, p. 1752.

[53] Schler, p. 1753.

[54] Rebecca Kysar, “The Senate Tax Plan Has a WTO Problem,” Medium, November 12, 2017, https://medium.com/whatever-source-derived/the-senate-tax-plan-has-a-wto-problem-guest-post-by-rebecca-kysar-31deee86eb99; Reuven S. Avi Yonah, “Guilty as Charged,” Tax Notes, 157 (8) (2017): 1134.

[55] Tom Bergin, “U.S. tax bill provision likely to spark EU trade dispute: legal experts,” Reuters, December 21, 2017, https://www.reuters.com/article/us-usa-tax-trade-analysis/u-s-tax-bill-provision-likely-to-spark-eu-trade-dispute-legal-experts-idUSKBN1EF24X.

[56] Kysar.

[57] Chuck Marr, Emily Horton, and Roderick Taylor, “IRS Budget Needs to Be Restored and Supplemented to Implement and Enforce the New Tax Law,” CBPP, January 25, 2018, https://www.cbpp.org/research/federal-tax/irs-budget-needs-to-be-restored-and-supplemented-to-implement-and-enforce-the.

[58] Emily Horton, “2018 Funding Bill Falls Short for the IRS,” CBPP, March 23, 2018, https://www.cbpp.org/blog/2018-funding-bill-falls-short-for-the-irs

[59] In this example, $300 million of the firm’s profits are booked overseas, with the remaining $200 million booked in the United States. This $200 million in U.S. profits is derived from the firm’s $3 billion in U.S. tangible assets, which amounts to a 6.7 percent rate of return. This rate of return is relatively modest, which could be caused by the operations associated with the firm’s tangible assets not generating that much value when they are isolated from the firm’s intellectual property (e.g., the bulk of the profits in the pharmaceutical industry come from patents, not the actual manufacturing of drugs). This rate of return also could reflect, at least in part, the incentive that companies have long had to overstate the share of profits coming from intellectual property, which is easier to shift to tax havens.

[60] The facts in this stylized example are obviously stark, but they are not that different in nature from arrangements that U.S. multinationals have entered into in the past. The purpose of this example is simply to demonstrate the incentives at work under the new law.

[61] Sections 250(a)(1)(B) and 78. This deduction is the mechanism by which the minimum tax is designed to yield a tax rate one-half the U.S. rate.

[62] Section 904 of the U.S. Internal Revenue code limits the amount of foreign taxes that generally can be claimed as a credit on the U.S. parent company’s tax return. In this case, however, the tentative tax credit of $13.3 million described in the fifth bullet is lower than the limit that section 904 imposes (which is $17.5 million) so all $13.3 million may be claimed as a credit. (There is some uncertainty surrounding the application of section 904 to the minimum tax, relating in particular to whether the interest expenses of the U.S. parent company should be allocated against foreign-source income. The stylized example above ignores this issue.) There is also some uncertainty about the “gross-up” that adds back the foreign taxes into the calculation of income, and whether it goes into the minimum tax’s foreign tax credit basket. This analysis assumes it does go into the minimum tax’s basket. See Elizabeth J. Stevens and H. David Rosenbloom, “GILTI Pleasures,” Tax Notes International, February 12, 2018, https://www.taxnotes.com/tax-notes-international/tax-reform/gilti-pleasures/2018/02/12/26vw0.

More from the Authors

Areas of Expertise

Areas of Expertise