States That Still Impose Sales Taxes on Groceries Should Consider Reducing or Eliminating Them

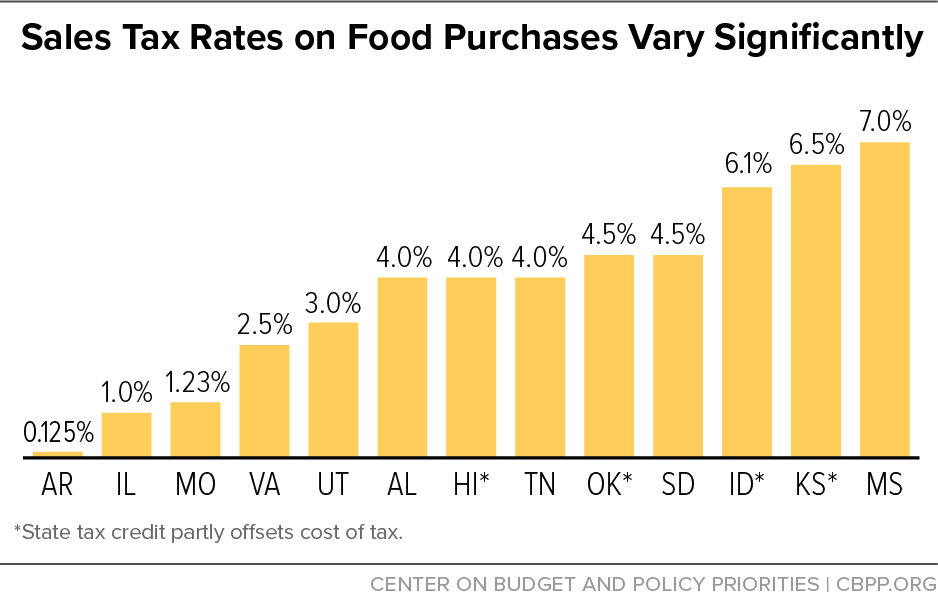

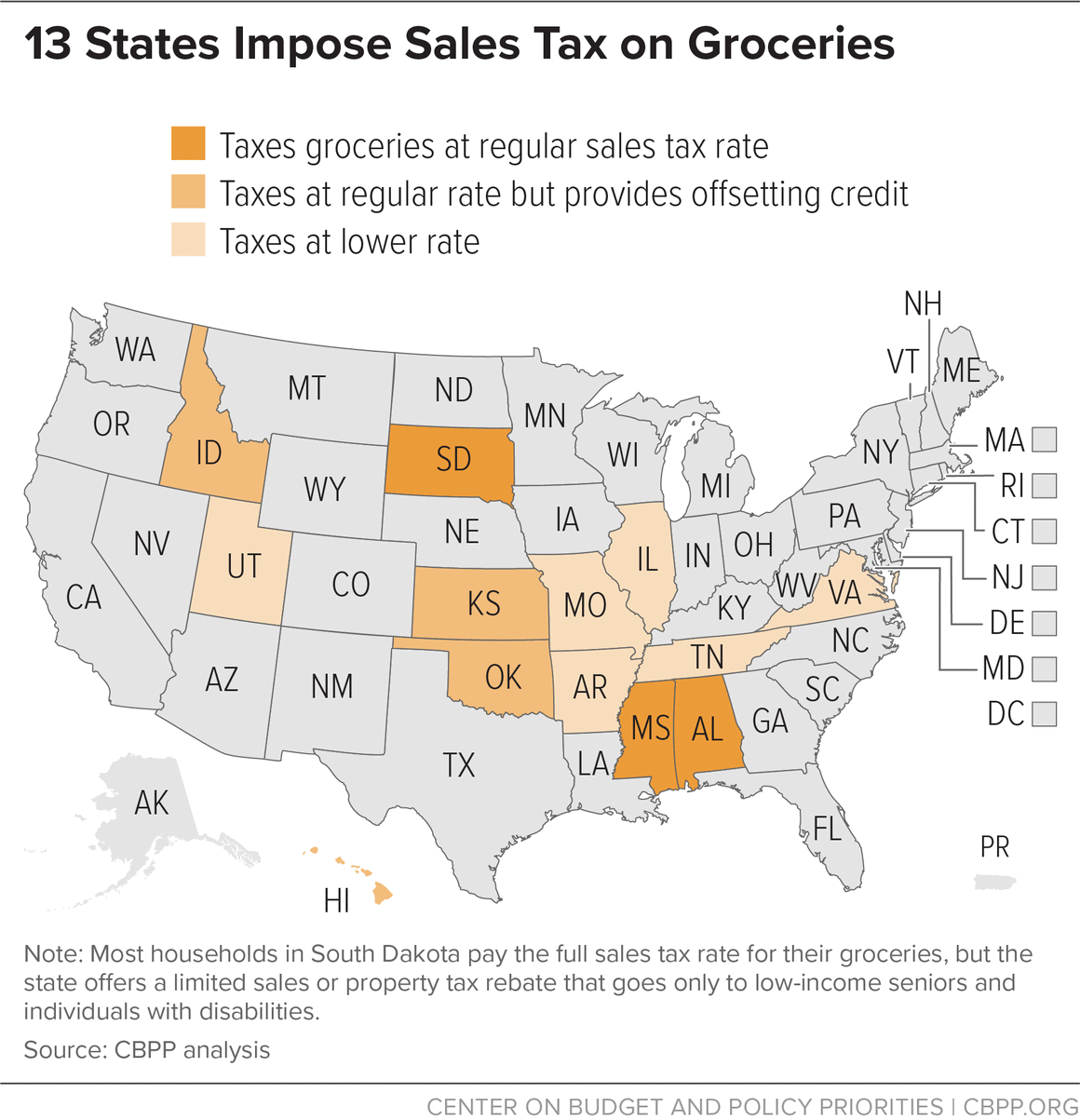

"Thirteen of the 45 states with a sales tax still impose it on groceries."State policymakers looking to make their tax codes more equitable should consider eliminating the sales taxes families pay on groceries if they haven’t already done so, or at least reducing these taxes or partially offsetting them through a tax credit.[1] Thirteen of the 45 states with a sales tax still impose it on groceries. (See Figure 1.) Of those, ten offer a lower tax rate for groceries than the general sales tax rate or provide a tax credit to offset some or all of the sales tax on groceries. Only Alabama, Mississippi, and South Dakota still tax groceries at the full state sales tax rate.

Sales taxes worsen income and racial inequalities.[2] Low-income people pay much more of their income in sales taxes than higher-income people do because they must spend a very large share of their income to meet basic needs. The lowest-income fifth of families (those making less than $20,800) — who are disproportionately families of color due to historical and contemporary discrimination — pay almost eight times more as a share of their incomes in sales taxes than the top 1 percent of families (those making more than $553,200), on average: 7.1 percent versus 0.9 percent.[3] The revenue systems in states that rely too heavily on sales taxes thereby create additional barriers for lower-income residents, making it harder for them, for example, to afford daily expenses like gas for their cars or to rent in neighborhoods with more opportunities — which, in turn, may make it more difficult for them to work their way into the middle class.

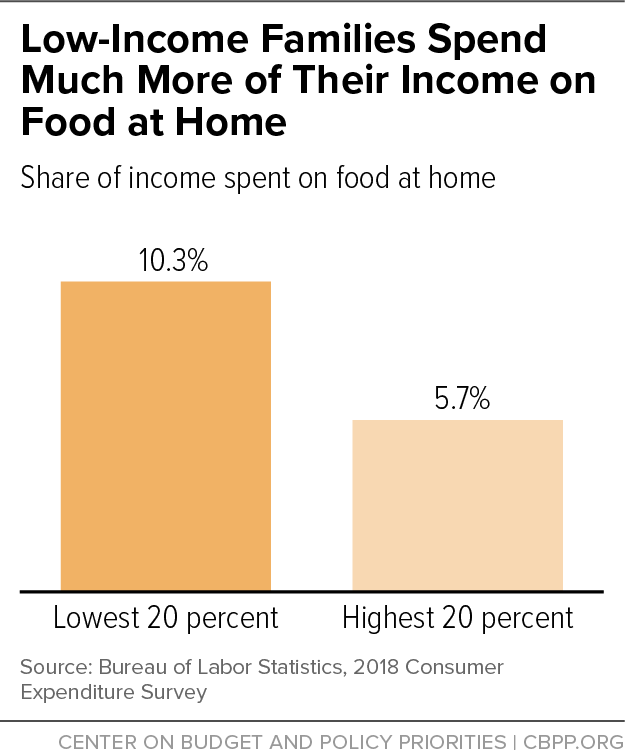

Sales taxes on groceries have an especially harmful impact on income and racial inequities since low-income families tend to spend a larger share of their income on groceries. The lowest-income fifth of families spend almost twice the share of their annual income on food at home that the highest-income fifth do: 10.3 percent versus 5.7 percent. (See Figure 2.) Overall, the higher the income bracket, the smaller the share spent on food at home. For the lowest-income families, food at home is the third-highest expenditure category as a share of income, after housing and transportation. For the highest-income families, it is the fifth, after housing, transportation, pension and Social Security contributions, and health care.[4]

Federal law exempts grocery purchases made using SNAP (food stamp) benefits from sales tax, but not all low-income families are eligible to receive SNAP benefits[5] and not all households that are eligible for SNAP participate.[6] Moreover, even when households do receive SNAP, for most their SNAP benefits do not cover all of their food purchases. First, SNAP benefit rules assume that a portion of a household’s other income will be used to purchase food.[7] For example, the typical working family with children that participated in SNAP in 2018 received a SNAP benefit of about $320 a month; the typical household with an elderly member received $120 a month. Other income (from earnings in the first case or Social Security in the second, or from other sources) would need to cover any food purchases above these households’ SNAP benefits. In addition, substantial research finds that SNAP benefit levels are not sufficient to meet the nutritional needs of most low-income households.[8] As a result, most SNAP households must use cash for a significant part of their grocery purchases since SNAP benefits usually don’t cover the full cost of a family’s basic diet.

Taxing groceries and then offering a tax credit to low-income families is less expensive for states than a full exemption but typically fails to offset grocery taxes for many people in poverty. These credits may be too small, available only to some low-income people, or require families to know about the credit and fill out a form or file taxes (even if they otherwise don’t need to) to apply for it.[9] In addition, the sales tax is paid at the time the food is purchased, but tax credits are paid annually in a lump sum, so they don’t help low-income families make ends meet on a monthly basis. Further, the value of these credits declines over time as food costs rise, since no state with a credit today adjusts it for inflation and some have not increased it in many years. For instance, Oklahoma’s credit of $40 per person in the household has not changed in at least three decades.

States that tax groceries or are considering doing so have better ways to raise the revenues needed for public investments. For example, states can eliminate tax breaks for special interests, raise tax rates for high-income households, or expand taxes on profitable corporations. They can also tweak their sales taxes to keep pace with a changing economy. Options include broadening the sales tax base to include more services, enacting an “Amazon law” to require large online retailers to collect sales taxes that are legally due on online purchases but that retailers otherwise aren’t required to collect, extending the sales tax to Internet downloads (such as software and music), and closing a tax loophole that allows online travel companies to collect taxes on only part of the sales taxes due on hotel room booking.[10]

The inclusion of food purchases in state sales taxes has also contributed to the long-term decline in sales tax revenue as a share of a state’s economy. That’s because spending on food for home consumption as a share of total spending has dropped dramatically over the past half century. In 2018, the average U.S. family spent just 7 cents of each consumption dollar on food for home consumption, down from 20 cents in 1960.[11]

States shifting away from grocery taxes in the past have often chosen to raise their sales tax rate to help pay for the loss of grocery tax revenue. This can raise substantial revenue but weakens the anti-poverty impact of eliminating grocery taxes, since sales taxes also fall hardest on low-income families as a share of income.

Most States Offer Tax Breaks for Groceries; Holdouts Should Follow Suit

Forty-five states plus the District of Columbia levy general sales taxes. Most have eliminated, reduced, or partially offset the tax as applied to food for home consumption. Of the states with sales taxes:

- Thirty-two states plus the District of Columbia exempt most food purchased for consumption at home from the state sales tax.

- Six states (Arkansas, Illinois, Missouri, Tennessee, Utah, and Virginia) tax groceries at lower rates than other goods.[12] (See Figure 3.) Most recently, Tennessee cut its sales tax on food to 4 percent from 5 percent in 2017; Arkansas cut its rate to 0.125 percent from 1.5 percent in 2019.

- Four states (Hawaii, Idaho, Kansas, and Oklahoma) tax groceries at the regular sales tax rate but offer credits or rebates offsetting some of the tax for some parts of the population. These credits or rebates usually are set at a flat amount per family member. As noted, credits are less expensive than a full exemption but also less effective at protecting low-income families from the impact of the tax.

- Three states (Alabama, Mississippi, and South Dakota) continue to apply their sales tax fully to food purchased for home consumption without providing any offset for low- and moderate-income families.[13]

Local governments, which in many states levy their own sales taxes, usually exempt food if food is exempt at the state level. Exceptions include localities in Arizona, Colorado, Georgia, Louisiana, North Carolina, and South Carolina, where grocery food purchases are fully or partially exempt at the state level but typically taxed at the local level. States considering new exemptions on grocery taxes need to decide whether to allow localities to continue taxing groceries, which would substantially weaken the benefits of the exemption for low-income families and create administrative challenges for businesses collecting the tax. Barring application of the sales tax to groceries in localities currently imposing the tax would reduce local government revenues, however, so states may wish to increase financial aid to localities or take other steps to help localities deal with the revenue loss.

In recent years, some states have considered repealing state sales taxes on groceries, while others have considered raising them. In 2017, the Idaho legislature passed a measure repealing the sales tax on groceries along with the corresponding tax credit, but Governor Butch Otter vetoed it.[14] In 2018, a bipartisan bill to repeal Utah’s tax on groceries cleared the House of Representatives but failed in the state Senate.[15] In terms of expansion proposals, New Mexico legislators have considered restoring the sales tax on groceries several times over the last few years, though none of these proposals became law.[16] The only state to increase its tax rate on groceries in recent years was Utah; in 2019, policymakers approved an increase in the state tax on groceries and created a refundable tax credit to offset part of the cost for people with modest incomes, as part of a broader tax package,[17] but they later repealed the package in response to public outcry.[18]

End Notes

[1] For more discussion of issues involving sales taxation of food, see Nicholas Johnson and Iris J. Lav, “Should States Tax Food? Examining the Policy Issues and Options,” Center on Budget and Policy Priorities, May 1998, https://www.cbpp.org/sites/default/files/atoms/files/stfdtax98.pdf.

[2] The term “sales tax” in this paper refers to general sales taxes on goods and services as defined by the Census Bureau in its Government Finances series. (See https://www.census.gov/programs-surveys/gov-finances/about/glossary.html#par_textimage_1654604272https://www.census.gov/programs-surveys/gov-finances/about/glossary.html#par_textimage_1654604272.) This definition includes most retail sales and use taxes but excludes nominal business license taxes as well as taxes that are levied specifically on such items as alcohol, tobacco, insurance products, motor fuels, amusements, and utilities. In several states, the sales tax is known in statute by another name.

[3] Institute on Taxation and Economic Policy, “Who Pays? A Distributional Analysis of the Tax Systems in All 50 States,” October 2018, https://itep.org/wp-content/uploads/whopays-ITEP-2018.pdf.

[4] U.S. Bureau of Labor Statistics, 2018 Consumer Expenditure Survey (released September 10, 2019), https://www.bls.gov/cex/tables.htm#annual.

[5] Some low-income households do not qualify for SNAP due to the program’s federal income or asset limits. Also, some categories of people are not eligible for SNAP regardless of how small their income or assets may be, such as many adults without children in the home, many college students, certain legal immigrants, and immigrants without documented status. For more on who is eligible for SNAP, see Center on Budget and Policy Priorities, “Policy Basics: The Supplemental Nutrition Assistance Program (SNAP),” updated June 25, 2019, https://www.cbpp.org/research/food-assistance/policy-basics-the-supplemental-nutrition-assistance-program-snap.

[6] About 15 percent of households that qualify for SNAP do not enroll. U.S. Department of Agriculture, “Trends in Supplemental Nutrition Assistance Program Participation Rates: Fiscal Year 2010 to Fiscal Year 2017,” September 2019, https://www.fns.usda.gov/snap/trends-supplemental-nutrition-assistance-program-participation-rates-fiscal-year-2010.

[7] The SNAP benefit formula assumes that 30 percent of a household’s “net” income (after a series of deductions to take into account certain other basic needs) will be used to purchase food. SNAP makes up the difference between the household’s expected contribution to food purchases and the cost of the “Thrifty Food Plan,” the Agriculture Department’s estimate of a diet intended to provide adequate nutrition at a minimal cost. See Center on Budget and Policy Priorities, “A Quick Guide to SNAP Eligibility and Benefits,” updated November 1, 2019, https://www.cbpp.org/research/food-assistance/a-quick-guide-to-snap-eligibility-and-benefits.

[8] For more on SNAP benefit levels, see Steven Carlson, “More Adequate SNAP Benefits Would Help Millions of Participants Better Afford Food,” Center on Budget and Policy Priorities, July 30, 2019, https://www.cbpp.org/research/food-assistance/more-adequate-snap-benefits-would-help-millions-of-participants-better.

[9] The eligibility criteria, amount, and refundability of the current credits vary widely. Hawaii, for instance, has a refundable credit that phases out for a single filer making over $30,000, but neither the income threshold nor the credit amount automatically adjusts to account for inflation, which shrinks the credit’s real value and reach over time. The credit also requires consumers to complete and submit a separate form with their tax return, which creates an additional barrier. The Kansas credit is nonrefundable and only applicable after all other credits have been utilized, so it provides little benefit to low-income filers, who often have little to no state income tax liability. Kansas’ credit is also only available to filers who are 55 and older, those with permanent disabilities, or those with a dependent under 18, which effectively excludes childless adults.

[10] For more on how states can update their sales taxes, see Michael Leachman and Michael Mazerov, “Four Steps to Moving State Sales Taxes Into the 21st Century,” Center on Budget and Policy Priorities, July 9, 2013, https://www.cbpp.org/research/state-budget-and-tax/four-steps-to-moving-state-sales-taxes-into-the-21st-century.

[11] Bureau of Labor Statistics data. For the 2018 figure, see https://www.bls.gov/cex/tables.htm#annual; for the 1960 figure, see https://www.bls.gov/cex/1961/Standard/ce_196061_tables.pdf.

[12] Food sales tax rates (and general sales tax rates) in these states are as follows: Arkansas: 0.125 percent (6.5 percent), Illinois: 1 percent (6.25 percent), Missouri: 1.225 percent (4.225 percent), Tennessee: 4 percent (7 percent), Utah: 3 percent (6.1 percent), and Virginia: 2.5 percent (5.3 percent).

[13] South Dakota offers a limited refund of either sales or property taxes to eligible seniors and disabled residents. Most households in the state pay the full sales tax rate on food.

[14] Idaho Legislature, 2017 regular legislative session, HB 67, https://legislature.idaho.gov/sessioninfo/2017/legislation/h0067/.

[15] Utah State Legislature, 2018 general session, HB 148, https://le.utah.gov/~2018/bills/static/HB0148.html. In 2019, Alabama considered — but did not adopt — a proposal to exempt groceries from taxation and to allow cities and counties to reduce or eliminate their sales taxes on groceries. John Sharp, “Grocery tax plan halted in Alabama House committee,” AL.com, April 17, 2019, https://www.al.com/news/2019/04/grocery-tax-plan-halted-in-alabama-house-committee.html.

[16] Rebecca Moss, “Food tax bills in New Mexico Legislature met with skepticism,” Santa Fe New Mexican, February 18, 2019, https://www.santafenewmexican.com/news/legislature/food-tax-bills-in-new-mexico-legislature-met-with-skepticism/article_d2e4fdd0-5cc5-5475-8146-c37314bc7fad.html. For more on attempts to restore the tax, see “Food Tax Repeal,” Think New Mexico, http://www.thinknewmexico.org/food-tax-repeal/.

[17] Utah State Legislature, 2019 second special session, SB 2001 Tax Restructuring Revisions, https://le.utah.gov/~2019S2/bills/static/SB2001.html.

[18] Bethany Rodgers and Benjamin Wood, “Utah’s Legislature, governor announce plans to repeal controversial tax reform law,” Salt Lake Tribune, January 24, 2020, https://www.sltrib.com/news/politics/2020/01/23/utahs-legislature/.

More from the Authors