BEYOND THE NUMBERS

Federal Report: ACA Dramatically Increased Health Coverage

The Affordable Care Act (ACA) dramatically improved health insurance coverage rates, and recent decisions by Congress and the Administration related to its implementation have boosted both coverage and affordability, according to a new report from the Department of Health and Human Services’ Assistant Secretary for Planning and Evaluation (ASPE).

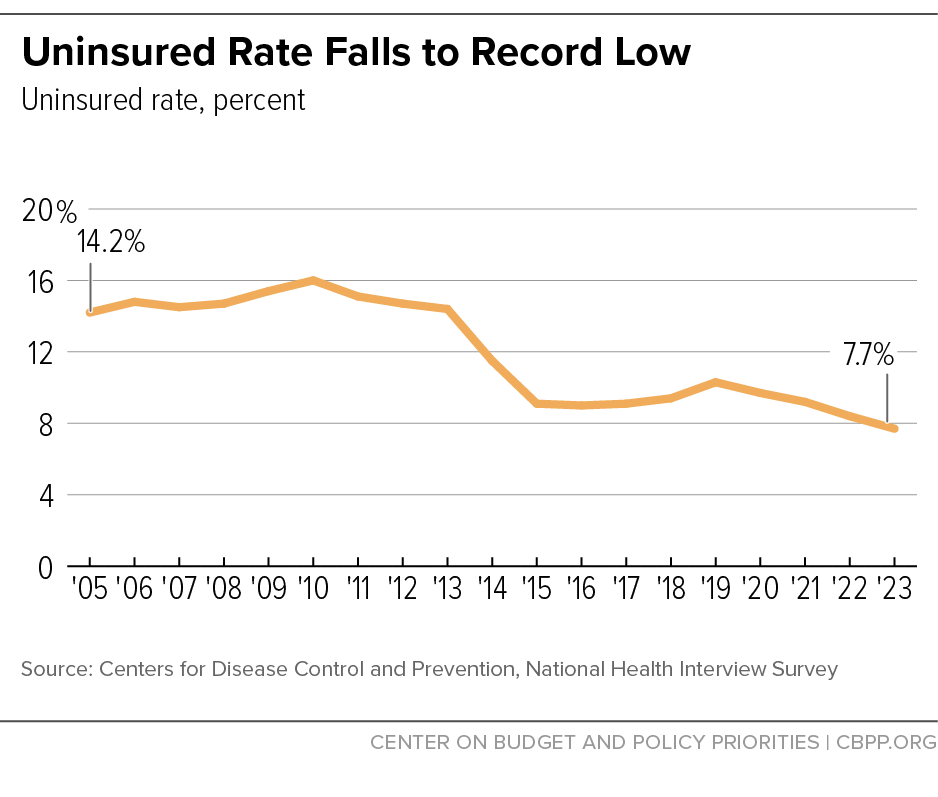

For many years before the ACA, the share of people with private health insurance coverage fell as rising health care costs made coverage increasingly unaffordable. Stringent Medicaid eligibility rules left non-disabled, low-income adults without children almost entirely without coverage options. By 2010, roughly 48 million Americans, or 16 percent of the population, lacked health insurance coverage.

Two key provisions of the ACA gave people new opportunities to access affordable, comprehensive coverage: tax credits for private coverage purchased through newly established marketplaces, and the expansion of Medicaid eligibility. The law also created federal standards for the private health insurance market, including guaranteeing coverage to people who have pre-existing health conditions and prohibiting insurers from charging higher premiums based on health status and gender.

The uninsured rate fell from 14.4 percent in 2013 (before the ACA’s major coverage expansions took effect in 2014) to 9.0 percent in 2016, the ASPE report notes. Insurance coverage rose in every state, with larger gains in states that expanded Medicaid.

Coverage gains were particularly strong for people with incomes under 200 percent of the federal poverty level. In states that adopted the Medicaid expansion after the Supreme Court gave states the choice whether to do so, Medicaid expansion provided eligibility for people with incomes below 138 percent of the federal poverty level. And in the ACA marketplaces, premium tax credits were largest for families with incomes between 100 and 200 percent of the federal poverty level. The ACA also reduced coverage inequities between racial and ethnic groups, between people living in rural and urban areas, and those related to sexual orientation and gender identity.

These gains were followed, however, by efforts to weaken the ACA that reduced coverage or made it less comprehensive or affordable between 2017 and 2020. After several legislative attempts to repeal the ACA failed, “the Trump administration undertook several administrative efforts to change the health insurance landscape…,” the ASPE report says. These included slashing federal funding for outreach and enrollment assistance that helps people navigate their coverage options and understand how much coverage will cost after premium tax credits are applied, discouraging people who are immigrants and their family members from enrolling in coverage, and expanding subpar plans that are exempt from ACA protections for people with pre-existing conditions.

Under federal guidance, some states implemented policies that reduced Medicaid enrollment, including premiums; policies that took away coverage from people who couldn’t complete paperwork showing that they are meeting or exempt from onerous work requirements; and other administrative burdens. Meanwhile, several additional states expanded Medicaid during this period, mitigating overall coverage losses.

In 2020, the COVID-19 pandemic prompted federal action to protect health coverage and support state budgets through legislation that increased federal Medicaid funding in states and ensured continuous coverage for Medicaid enrollees. These policies prevented people from losing coverage during the pandemic and helped drive down the uninsured rate.

Since 2021, legislative and administrative changes have built on the ACA, improving coverage and affordability and more than offsetting the coverage loss that occurred between 2017 and 2020, the ASPE report finds. As of 2023, the national uninsured rate had fallen below 8 percent, a record low that is less than half the rate before the ACA (see chart). The number of people with marketplace coverage has increased each year since 2021, with millions more people now enrolled.

Improvements to the premium tax credits for marketplace coverage helped increase marketplace enrollment to over 21 million in 2024, up nearly 80 percent since the improvements were first enacted in 2021, when enrollment stood at just 12 million. A record 92 percent of marketplace enrollees, or 19.7 million people, qualified for premium tax credits in 2024. These tax credits narrow inequities and improve coverage rates by providing upfront financial assistance to help people afford the health insurance plans offered in their state through the ACA marketplaces.

Increased investment in outreach and enrollment and the creation of additional time for people to enroll in marketplace coverage, called special enrollment periods, also contributed to the growth. Going forward, the Administration recently completed a regulation that will allow people with DACA status — Deferred Action for Childhood Arrivals — to access coverage and premium tax credits through the marketplace.

Important steps in Medicaid have also shored up coverage. States now have the option to provide 12 months of postpartum Medicaid coverage and are required to provide at least 12 months of continuous eligibility for children — protecting new parents and children from gaps in coverage, which are associated with poor health outcomes. A final rule released in 2024 simplifies Medicaid and Children’s Health Insurance Program eligibility requirements, streamlines application processes, and removes unnecessary administrative barriers to enrollment.

Enrollment in Medicaid has grown as four more states have adopted the ACA Medicaid expansion since 2021. Federal legislation made permanent federal fiscal incentives initially enacted in 2020 for states that newly expand Medicaid.

Opportunities to build on the ACA’s historic coverage gains remain, including expanding Medicaid in the ten remaining non-expansion states, reducing barriers to coverage for people who are immigrants, continued investment in outreach and enrollment assistance, and reducing administrative barriers to coverage. Critically, enhanced premium tax credits are set to expire after 2025. If Congress does not act, nearly all marketplace enrollees will face significantly higher premium costs and 4 million people could become uninsured.