The Pass-Through Deduction Is Skewed to the Rich, Costly, and Failed to Deliver on Its Promises

Deduction Should Expire as Scheduled

The 2017 Trump tax law was skewed to the rich, eroded the revenue base, and failed to deliver its promised economic benefits.[1] Few provisions of the law exemplify these flaws better than the 20 percent pass-through deduction, and policymakers should reject any efforts to extend the provision when it expires in 2025.

The centerpiece of the 2017 tax law was its permanent cut in the corporate tax rate from 35 percent to 21 percent, which has proven very costly. But more than half of business income flows to businesses organized as pass-through entities (such as partnerships, S corporations, and sole proprietorships),[2] which are not subject to the corporate tax. Instead, their income “passes through” the business and is reported on owners’ individual tax returns.

Before the 2017 tax law, this income was generally taxed at the same rates as wage and salary income; wages and salaries are taxed at a top rate of 37 percent under the 2017 tax law. Because the corporate rate reduction did not affect these owners, business lobbyists argued that a special pass-through tax break was needed to maintain “parity” with corporations. As a result, the law added the pass-through deduction, which effectively cuts the top tax rate on this pass-through income by a fifth, to 29.6 percent. But this parity argument has always been misguided — and misleading — and the deduction lacks a solid policy rationale. (See box.)

The pass-through deduction:

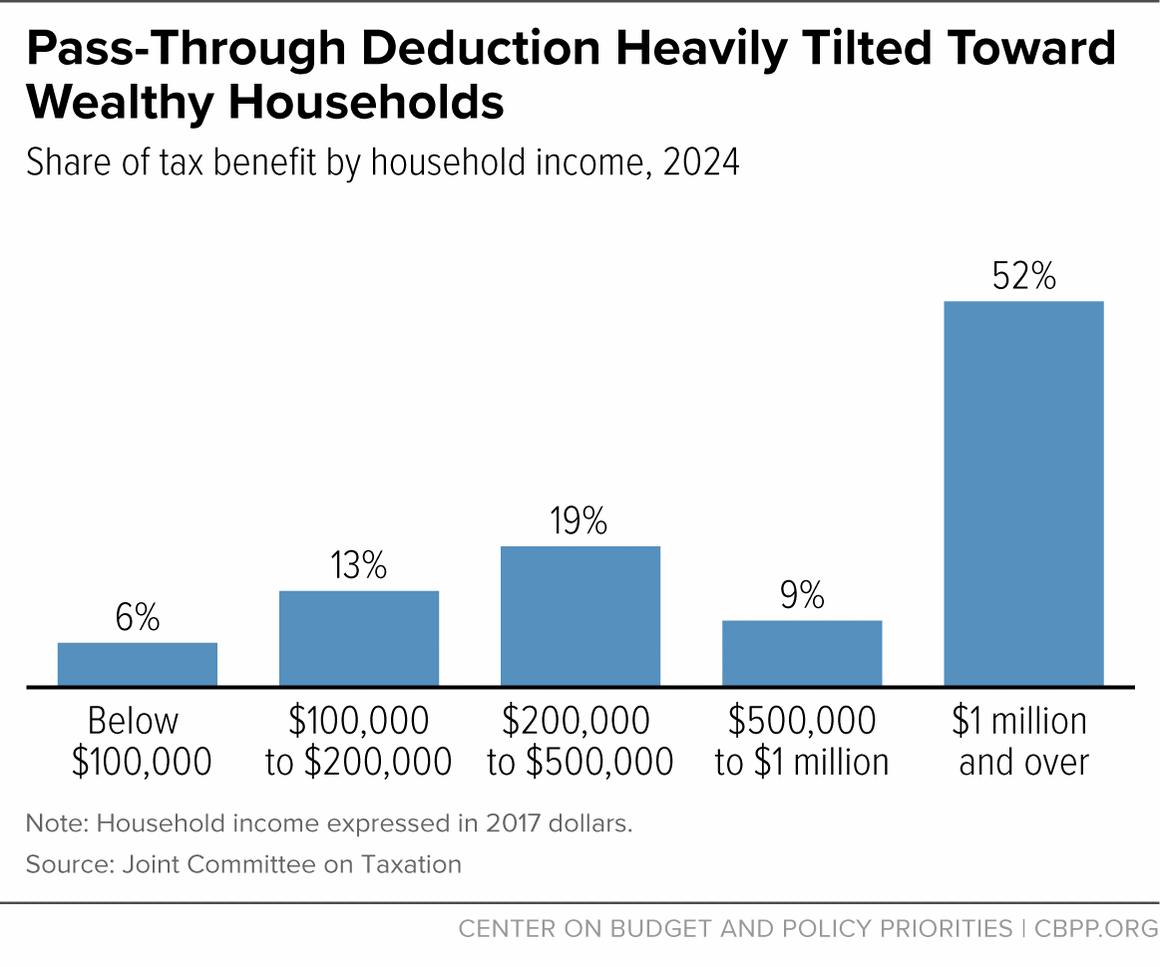

- Is skewed to the rich: Over half of the deduction’s benefits in 2024 will go to households with more than $1 million in income, according to the Joint Committee on Taxation (JCT).[3]

- Costs significant revenue: Extending this provision beyond its scheduled expiration at the end of 2025 would cost around $770 billion over the decade that would follow.[4]

- Has failed to deliver on its economic promises: Proponents argued the pass-through deduction would boost investment and create jobs.[5] Then-Treasury Secretary Steven Mnuchin, for example, argued the deduction would “be good for the economy; good for growth.”[6] But a team of researchers from the Treasury, the Federal Reserve, and academia concluded that the deduction’s benefits have largely failed to trickle down to workers who aren’t owners and did not provide any significant boost in economic activity.[7]

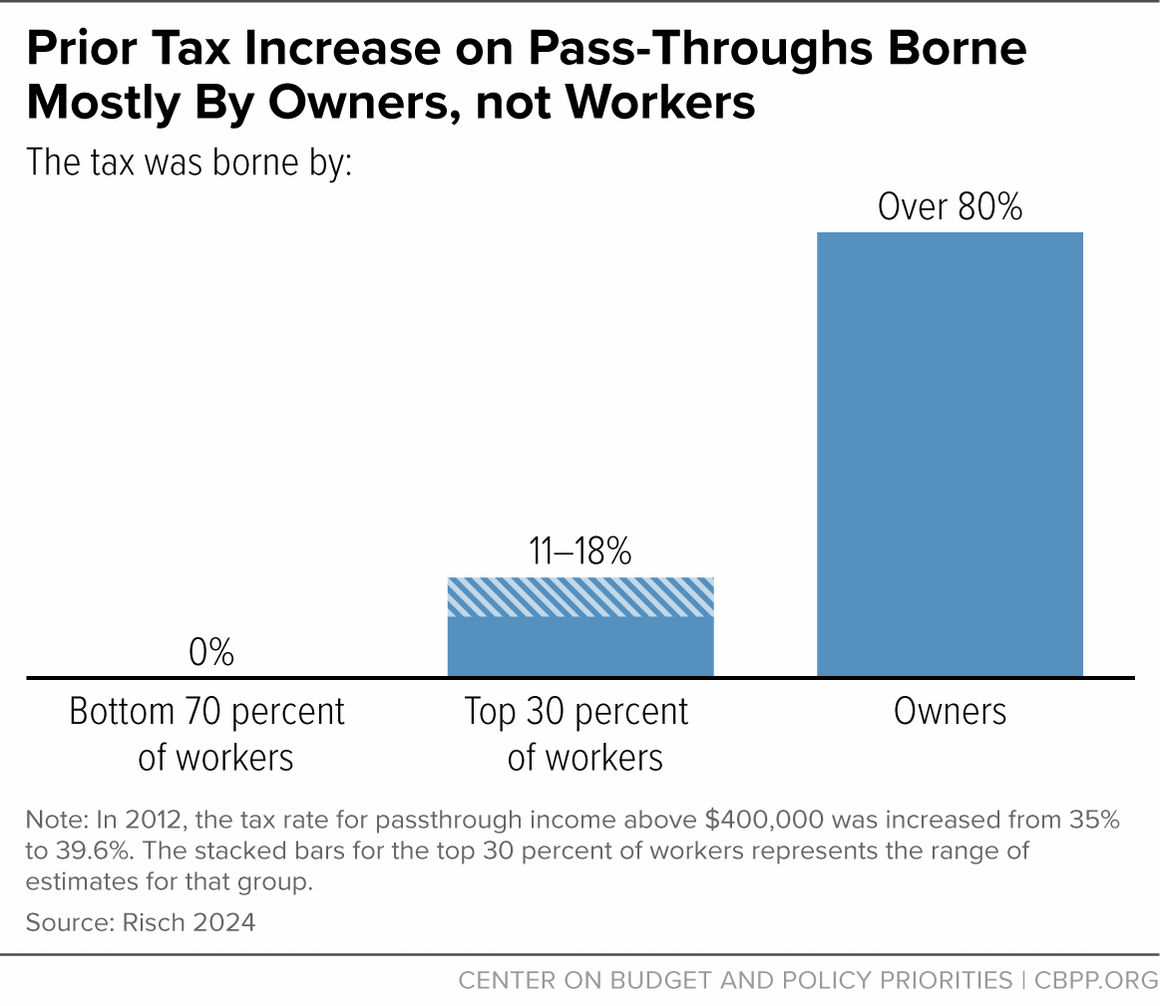

In addition to the research showing the failure of the pass-through deduction to deliver broad economic benefits, rigorous research shows that policy moving in the opposite direction — that is, raising the tax rate on pass-through owners — does not harm most workers or the broader economy. A recent paper by Carnegie Mellon economist Max Risch examines the effects of raising the top tax rate on pass-through business owners (those with incomes above $400,000) from 35 percent to 39.6 percent, a provision in the 2012 American Taxpayer Relief Act. Owners bore over 80 percent of the tax increase, and top-earning workers bore the remainder, Risch found. None of the burden fell on workers in the bottom 70 percent of the earnings distribution in the sample, and the tax increase had no impact on employment.[8]

While the pass-through deduction has failed to boost investment or create jobs, it has encouraged more tax gaming, leading more owners to reclassify their income as pass-through income that qualifies for the deduction.[9] This is one of the worst kinds of tax policy: one that elicits little change in real economic activity but sparks a reclassification of existing activity. In the process it weakens the integrity of the entire income tax and drains the Treasury.

The skewed nature of the pass-through deduction, its large expense and lack of economic benefits, and its invitation for gaming make an overwhelming case for its expiration. New York University law professor Daniel Shaviro has termed the deduction “the worst provision ever even to be seriously proposed in the history of the federal income tax.”[10] It should end as scheduled in 2025.

The Pass-Through Deduction Is Skewed to the Rich

Though the 2017 Trump tax law’s proponents often characterize the pass-through deduction as a tax break for small businesses, large businesses also benefit from the deduction and claim a disproportionate share of the overall tax break.[11] The deduction is heavily skewed in favor of people with high incomes for the following reasons:

- Wealthy people are much more likely to have pass-through income than other people. For example, people in the top 1 percent are over 50 times more likely to have partnership income than people in the bottom 50 percent of the income spectrum.[12]

- Pass-through income is heavily tilted. In 2019, the latest non-pandemic year for which data are available, the average pass-through deduction across all taxpayers who claimed the deduction was roughly $7,000, but it was nearly $1 million for the 15,000 taxpayers with incomes above $10 million who claimed the deduction.[13]

- Because the provision is designed as a tax deduction rather than a tax credit, its relative value is much higher for wealthy pass-through owners. The value of a tax deduction equals the deduction amount times the taxpayer’s tax rate. For example, the same $1,000 pass-through deduction is currently worth $150 to someone with a modest income in the 15 percent bracket but $370 for a rich person in the top 37 percent bracket.

As a result, over half of the deduction’s benefits will go to households with more than $1 million in income in 2024, according to JCT.[14] (See Figure 1.)

The pass-through deduction widens racial and ethnic inequities in after-tax income. Researchers at the Treasury Department estimated in 2023 that 90 percent of the benefit of the pass-through deduction accrues to white households while Hispanic and Black families receive 5 and 2 percent of the benefit, respectively.[15] (White households make up 67 percent of the total population, Hispanic households 15 percent, and Black households 11 percent.) The researchers do not explore why these inequities occur, but as mentioned above, the pass-through deduction disproportionately benefits high-income households. Non-Hispanic white households are heavily overrepresented among high-income households, while households of color are overrepresented among lower-income households due to racial and ethnic barriers to economic opportunity.

The Pass-Through Deduction Is Expensive and Has Failed to Deliver on Its Promises

Permanently extending the pass-through deduction would cost around $770 billion from 2026 to 2035.[16]

Proponents argued that the pass-through deduction would boost investment and create jobs. Then-Treasury Secretary Steven Mnuchin, for example, argued the deduction would “be good for the economy; good for growth.”[17] But researchers have found no evidence that it provided any significant boost in economic activity, increased investment, or broadly benefited non-owner workers. A team of economists, including from the Treasury and the Federal Reserve, found no evidence that the deduction led to additional investment, job growth, or higher wages for employees of pass-through businesses.[18]

This failure of the pass-through deduction to trickle down to the vast majority of workers should not be surprising given the track record of past trickle-down tax cuts for pass-through business owners. For example, studies of an even deeper tax cut for pass-through businesses in Kansas — a full exemption from state taxation — found that “the reform failed to generate real economic responses.”[19]

Another recent study followed pass-through businesses and their workers for several years after a tax increase and found a broadly similar result — that the change only affected owners and higher-paid workers and not other workers or economic activity at impacted companies.[20] This research looked at the effect of raising taxes on pass-through owners using the 2012 increase in the top marginal tax rate from 35 percent to 39.6 percent, which applied to pass-through income.

Business owners bore over 80 percent of the tax increase, the study found. The small share of the tax borne by employees was concentrated among those in the top 30 percent of the earnings distribution in the sample; most workers were unaffected. (See Figure 2.) Meanwhile, the study found no effects on sales, employment, or productivity at businesses subject to the higher top tax rate. The author, Carnegie Mellon economist Max Risch, offers “rent sharing” between owners and higher-paid workers as one explanation for the findings, meaning the tax burden falls on profits that firms tend to share with top earners.[21]

This suggests that just as the pass-through deduction has had no discernible economic upside, its expiration would have little to no economic downside.

Extending the Deduction Would Encourage Even More Gaming

While the pass-through deduction has not elicited much change in real economic activity, it has encouraged reclassification of the income and tax consequences of existing activity. This reclassification, which can verge on outright evasion, will continue and likely increase unless policymakers let this poorly designed provision expire as scheduled.

One form of partnership compensation that doesn’t benefit from the deduction, “guaranteed payments,” fell by roughly 30 percent in 2018, immediately after the 2017 tax law took effect.[22] It stayed low in 2019 as owners and their tax advisors took advantage of the arbitrary distinctions between types of income in the deduction’s complicated rules.[23] Partnerships often make guaranteed payments to partners (analogous to salaries). But if the partnership instead distributes the same amount of payments to partners as profits, those profits can qualify for the deduction. As a result of the new law, partnerships could increase their deductions simply by changing the distribution routes of the same income.

Researchers have also found evidence that some high-income pass-through business owners in industries that are excluded from the deduction — such as law or consulting — may artificially change their self-reported industry classification on their tax returns to attempt to claim the deduction.[24] For example, 6 percent of owners of S corporations who called themselves “consultants” before the 2017 tax law — an industry that is disqualified from the deduction above certain income thresholds — reported being in a qualifying industry after the deduction went into effect.[25] This type of artificial reclassification does not affect whether a business owner may legally claim the deduction, but the IRS would have to conduct a time- and resource-intensive audit of a business to determine whether its purported industry classification matches its true business type.

If the deduction is made permanent, high-income taxpayers will increasingly reclassify their income as pass-through income; this tax distortion will grow and grow. The Tax Policy Center estimated that this type of gaming could account for around 16 percent of the total revenue loss over 2026-2040 from extending the deduction.[26]

The large accounting changes that the deduction promotes often have no economic basis, are a drain on the Treasury, and can even be illegal but resource-intensive for the IRS to detect. Complex and valuable tax benefits like the pass-through deduction encourage taxpayers to push the boundary between lawful tax avoidance — itself engaged in by people with access to well-paid tax advisors — and unlawful evasion.

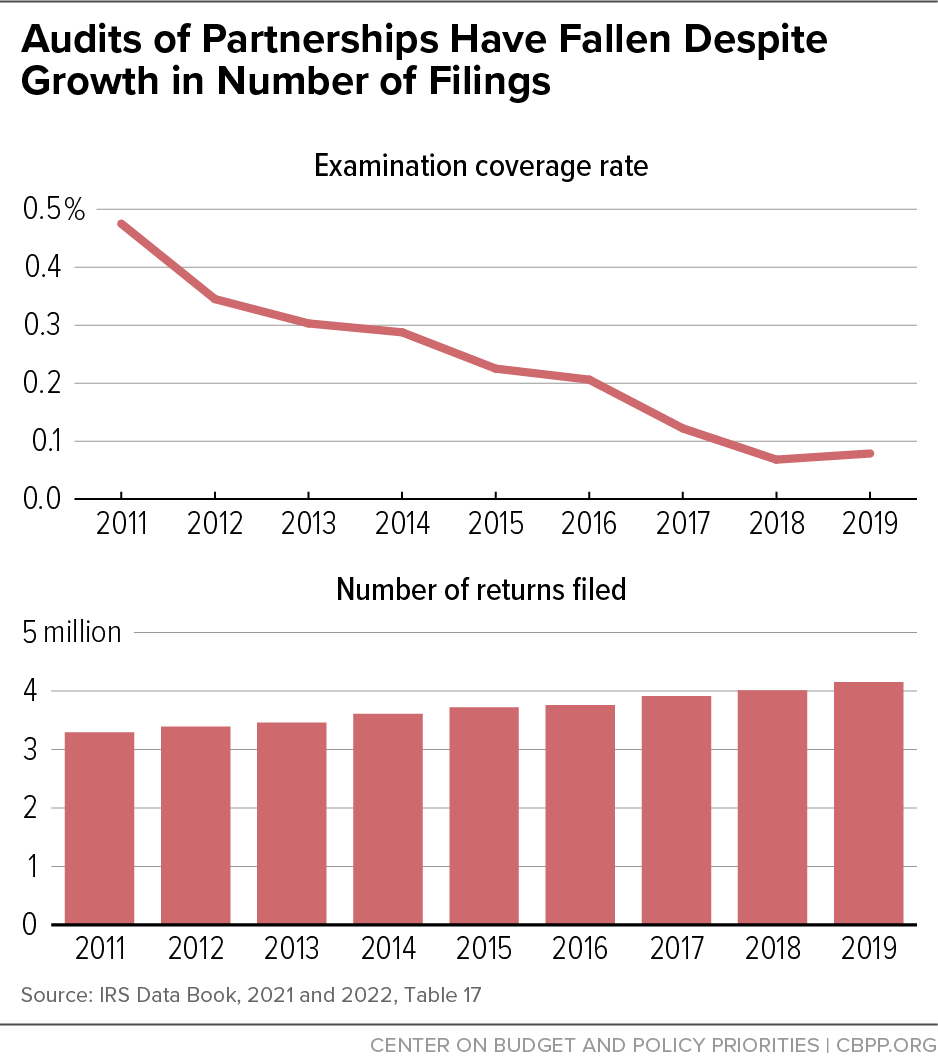

Plummeting pass-through audit rates give them more leeway to do so.Fewer than 0.1 percent of partnerships, for example, are audited each year.[27] (See Figure 3.) This weakens the integrity of the entire income tax and adds new burdens to an IRS that has struggled to adequately combat sophisticated tax evasion schemes involving pass-through entities.

The increased IRS enforcement funding provided by the Inflation Reduction Act will help the agency combat tax evasion of complex pass-throughs. But the IRS will continue to face challenges in detecting these schemes, and the returns for businesses that engage in them will remain tantalizingly large. Moreover, packing the tax code with invitations for illegal evasion only makes the IRS’s job of enforcing the tax code harder and more costly. This is yet another reason that the pass-through deduction should expire as scheduled in 2025.[28]

Instead of extending ineffective and costly tax cuts that invite tax evasion and benefit wealthy households, policymakers should raise revenues through progressive tax policies and use them to finance high-return public investments that can promote broadly shared growth and reduce future economic risk associated with high levels of debt. For example, compelling research finds that in addition to short-run relief from hardship, income support can bring long-run gains in children’s health, education, and earnings,[29] supporting a strong economy and better positioning everyone to thrive. This is just one area in which federal investment remains far short of need. Policymakers should support such policies instead of continuing skewed, costly tax breaks like the pass-through deduction.

End Notes

[1] Chuck Marr, Samantha Jacoby, and George Fenton, “The 2017 Trump Tax Law Was Skewed to the Rich, Expensive, and Failed to Deliver on Its Promises,” CBPP, March 5, 2024, https://www.cbpp.org/research/federal-tax/the-2017-trump-tax-law-was-skewed-to-the-rich-expensive-and-failed-to-deliver.

[2] David S. Mitchell, “Factsheet: What the research says about taxing pass-through businesses,” Washington Center for Equitable Growth, April 30, 2024, https://equitablegrowth.org/factsheet-what-the-research-says-about-taxing-pass-through-businesses/#footnote-1.

[3] Joint Committee on Taxation, “Tables Related to the Federal Tax System as in Effect 2017 through 2026,” JCX-32r-18, April 24, 2018, https://www.jct.gov/publications/2018/jcx-32r-18/.

[4] CBPP analysis of Congressional Budget Office (CBO) May 2024 estimates of the effects of extending the 2017 tax law’s expiring individual and estate tax provisions over the 2025-2034 period. See CBO, “Budgetary Outcomes Under Alternative Assumptions about Spending and Revenues,” May 8, 2024, https://www.cbo.gov/publication/60114.

[5] Steven Mufson, “Sen. Johnson is a ‘no’ on the tax bill. He says it hurts businesses (like his own),” Washington Post, November 16, 2017, https://www.washingtonpost.com/business/economy/sen-johnson-is-a-no-on-the-tax-bill-he-says-it-hurts-businesses-like-his-own/2017/11/16/c47b2a56-ca54-11e7-b0cf-7689a9f2d84e_story.html.

[6] Matthew J. Belvedere, “Mnuchin: GOP tax reform would give small business owners the lowest rates ‘since the 1930s,’” CNBC, November 17, 2017, https://www.cnbc.com/2017/11/17/mnuchin-gop-tax-plan-gives-small-business-lowest-rates-since-1930s.html.

[7] Lucas Goodman et al., “How Do Business Owners Respond to a Tax Cut? Examining the 199A Deduction for Pass-through Firms,” NBER Working Paper 28680, January 2024,https://www.nber.org/system/files/working_papers/w28680/w28680.pdf.

[8] Max Risch, “Does Taxing Business Owners Affect Employees: Evidence from a Change in the Top Marginal Tax Rate,” Quarterly Journal of Economics, February 2024, https://academic.oup.com/qje/article-abstract/139/1/637/7260871.

[9] Goodman et al, op. cit.

[10] Daniel Shaviro, “Apparently income isn’t just income any more,” December 16, 2017, https://danshaviro.blogspot.com/2017/12/apparently-income-isnt-just-income-any.html.

[11] Mitchell, op. cit.

[12] Michael Cooper et al., “Business in the United States: Who Owns it and How Much Tax Do They Pay?” NBER Working Paper 21651, October 2015, https://www.nber.org/papers/w21651. The study used data from 2011, when the top 1 percent began at about $375,000 in adjusted gross income.

[13] IRS Statistics of Income, 2019, https://www.irs.gov/pub/irs-prior/p1304--2021.pdf. During the pandemic-induced recession, household and business incomes rapidly declined; tax data are not representative of a typical year.

[14] Joint Committee on Taxation, op. cit.

[15] Julie-Anne Cronin, Portia DeFilippes, and Robin Fisher, U.S. Treasury Department Office of Tax Analysis, “Tax Expenditures by Race and Hispanic Ethnicity: An Application of the U.S. Treasury Department’s Race and Hispanic Ethnicity Imputation,” January 2023, https://home.treasury.gov/system/files/131/WP-122.pdf.

[16] CBPP analysis of the CBO May 2024 estimates of the effects of extending the 2017 tax law’s expiring individual and estate tax provisions over the 2025-2034 period. See CBO, op. cit. Moreover, if the pass-through deduction is extended while other 2017 law provisions are allowed to expire, the revenue costs of extending the deduction would likely rise because of the interaction between higher marginal rates with the deduction.

[17] Belvedere, op. cit.

[18] Goodman et al, op. cit.

[19] Jason DeBacker et al., “The Impact of State Taxes on Pass-Through Businesses: Evidence from the 2012 Kansas Income Tax Reform,” September 29, 2017, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2958353. See also Michael Mazerov, “Kansas Provides Compelling Evidence of Failure of ‘Supply-Side’ Tax Cuts,” CBPP, January 22, 2018, https://www.cbpp.org/research/kansas-provides-compelling-evidence-of-failure-of-supply-side-tax-cuts.

[20] Risch, op. cit.

[21] For further discussion of the role of rents in the corporate sector, see Chuck Marr, George Fenton, and Samantha Jacoby, “Congress Should Revisit 2017’s Trillion-Dollar Corporate Tax Cut in 2025,” CBPP, March 21, 2024, https://www.cbpp.org/research/federal-tax/congress-should-revisit-2017-tax-laws-trillion-dollar-corporate-rate-cut-in.

[22] Goodman et al., op. cit.

[23] Ibid.

[24] Goodman et al, op. cit.

[25] Ibid.

[26] Benjamin R. Page et al., “Tax Incentives for Pass-Through Income,” Tax Policy Center, July 15, 2020, https://www.taxpolicycenter.org/publications/tax-incentives-pass-through-income. This analysis assumes the 2017 tax law’s other expiring individual income tax provisions are allowed to sunset as scheduled.

[27] Internal Revenue Service, “Statistics of Income Data Book,” 2022, Table 17, https://www.irs.gov/pub/irs-pdf/p55b.pdf.

[28] Joint Committee on Taxation, “List of Expiring Federal Tax Provisions 2022-2034,” JCX-1-23, January 18, 2023, https://www.jct.gov/publications/2023/jcx-1-23/.

[29] Irwin Garfunkel et al., “The Benefits and Costs of a U.S. Child Allowance,” NBER Working Paper No. 29854, 2022, https://www.nber.org/papers/w29854; Andrew Barr, Jonathan Eggleston, and Alexander A. Smith, “Investing in Infants: the Lasting Effects of Cash Transfers to New Families,” Quarterly Journal of Economics, April 20, 2022, https://academic.oup.com/qje/article/137/4/2539/6571263.

More from the Authors

Areas of Expertise

Areas of Expertise